As filed with the U.S. Securities and Exchange Commission on June 8, 2023.

Registration No. 333-

United Mexican States (State or other jurisdiction of incorporation or organization) | | | 6500 (Primary Standard Industrial Classification Code Number) | | | None (I.R.S. Employer Identification No.) |

Maurice Blanco Manuel Garciadiaz Drew Glover Davis Polk & Wardwell LLP 450 Lexington Avenue New York, New York 10017 +1 (212) 450-4000 | | | Juan Francisco Mendez Simpson Thacher & Bartlett LLP 425 Lexington Avenue New York, New York 10017 +1 (212) 455-2000 |

| | | Per ADS | | | Total | | | Per Common Share | | | Total | |

Public offering price | | | US$ | | | US$ | | | US$ | | | US$ |

Underwriting discounts and commissions(1)(2) | | | US$ | | | US$ | | | US$ | | | US$ |

Proceeds, before expenses, to us(2) | | | US$ | | | US$ | | | US$ | | | US$ |

(1) | See “Underwriting” for a description of the compensation payable to the underwriters. |

(2) | Assumes no exercise of the underwriters’ over-allotment option. |

Citigroup | | | BofA Securities | | | Barclays |

Morgan Stanley | | | Scotiabank |

| | | Page | |

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | |

• | our business and strategy of investing in industrial facilities, which may subject us to risks of the sector in which we operate but uncommon to other companies that invest primarily in a broader range of real estate assets; |

• | our ability to maintain or increase our rental rates and occupancy rates; |

• | the performance and financial condition of our tenants; |

• | our expectations regarding income, expenses, sales, operations and profitability; |

• | our ability to obtain returns from our projects similar or comparable to those obtained in the past; |

• | our ability to successfully expand into new markets in Mexico; |

• | our ability to successfully engage in property development; |

• | our ability to lease or sell any of our properties; |

• | our ability to successfully acquire land or properties to be able to execute on our accelerated growth strategy; |

• | the competition within our industry and markets in which we operate; |

• | economic trends in the industries or the markets in which our customers operate; |

• | the continuing impact of the coronavirus pandemic identified as SARS-CoV-2 (“COVID-19”) and the impact of any other pandemics, epidemics or outbreaks of infectious diseases on the Mexican economy and on our business, results of operations, financial condition, cash flows and prospects, as well as our ability to implement any necessary measures in response to such impact; |

• | higher interest rates, increased leasing costs, increased construction costs, distressed supply chains for construction materials, increased maintenance costs, all of which could increase our costs and limit our ability to acquire or develop additional real estate assets; |

• | the terms of laws and government regulations that affect us, and interpretations of those laws and regulations, including changes in tax laws and regulations and changes in environmental, real estate and zoning laws; |

• | supply of utilities, principally electricity and water, and general availability of public services, to support operations in our properties and industrial parks; |

• | economic, political and social developments in Mexico, including political instability, currency devaluation, inflation, and unemployment; |

• | the performance of the Mexican economy and the global economy; |

• | the competitiveness of Mexico as an exporter of manufactured and other products to the United States and other key markets; |

• | limitations on our access to sources of financing on competitive terms; |

• | changes in capital markets that might affect the investment policies or attitude in Mexico or regarding securities issued by Mexican companies; |

• | obstacles to commerce, including tariffs or import taxes and changes to the existing commercial policies, and change or withdrawal from free trade agreements, including the USMCA, of which Mexico is a member that might negatively affect our current or potential clients or Mexico in general; |

• | increase of trade flows and the formation of trade corridors connecting certain geographic areas of Mexico and the U.S., which results in a vigorous economic activity within those areas in Mexico and a source of demand for industrial buildings; |

• | our ability to execute our corporate strategies; |

• | the growth of e-commerce markets; |

• | a negative change in our public image; |

• | epidemics, catastrophes, insecurity and other events that might affect the regional or national consumption; |

• | the loss of key executives or personnel; |

• | restrictions on foreign currency convertibility and remittance outside Mexico; |

• | changes in exchange rates, market interest rates or the rate of inflation; |

• | possible disruptions to commercial activities due to natural and human-induced disasters that could affect our properties in Mexico, including criminal activity relating to drug trafficking, terrorist activities, and armed conflicts; |

• | deterioration of labor relations with third-party contractors, changes in labor costs and labor difficulties, including subcontracting reforms in Mexico comprising changes to labor and social laws; |

• | the prices of our common shares or ADSs may be volatile or may decline regardless of our operational performance; |

• | the increased costs and disruptions to our business arising from our transformation into a public company in the United States; and |

• | other risk factors included under “Risk Factors” in this prospectus. |

| | | As of March 31, | | | As of December 31, | ||||

| | | 2023 | | | 2022 | | | 2021 | |

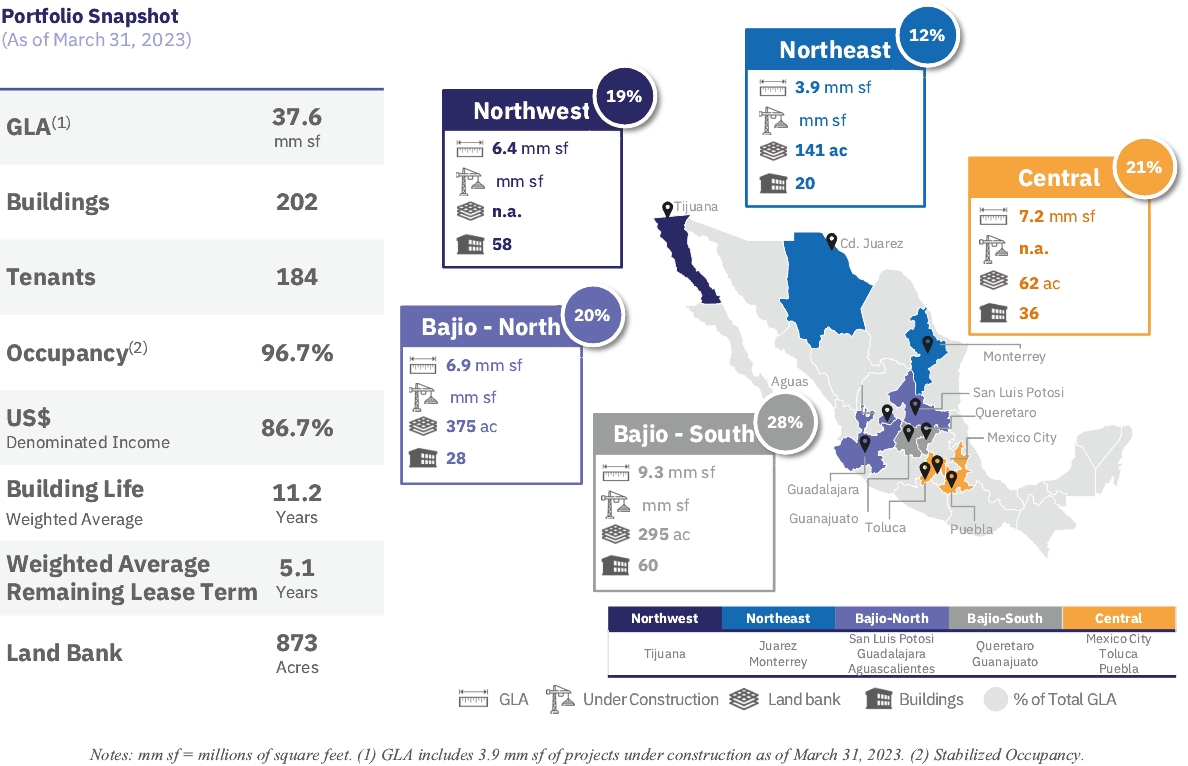

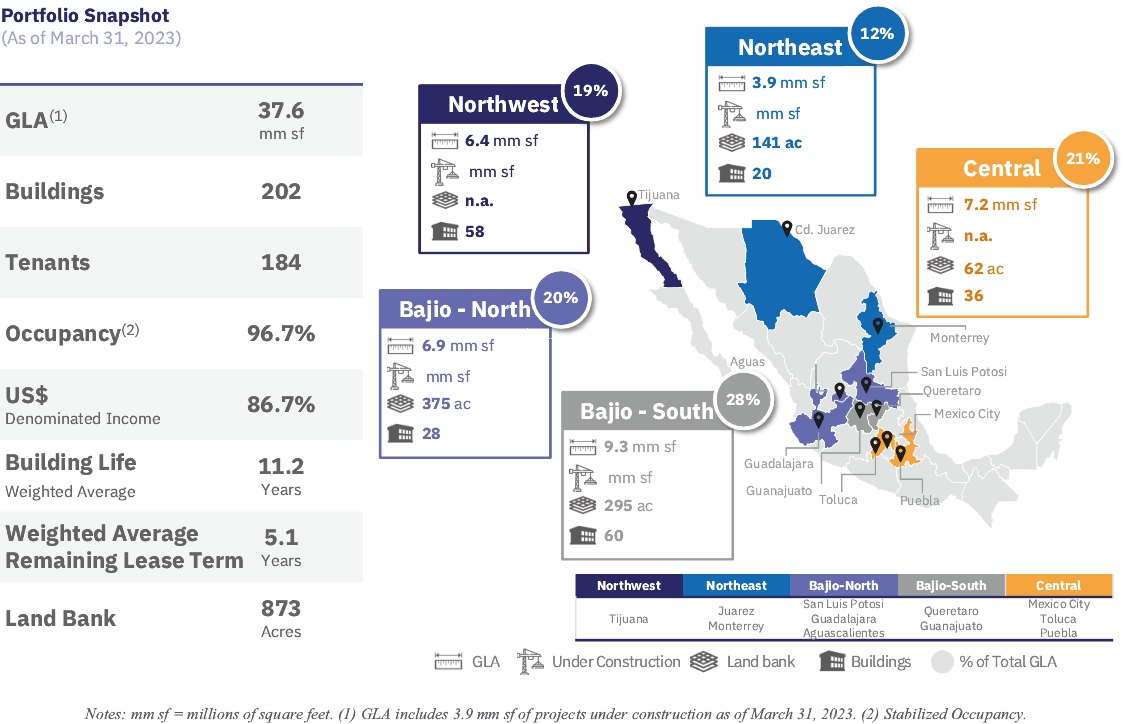

Number of real estate properties | | | 202 | | | 202 | | | 189 |

GLA (sq. feet)(1) | | | 33,714,370 | | | 33,714,370 | | | 31,081,746 |

Leased area (sq. feet)(2) | | | 32,064,157 | | | 32,054,026 | | | 29,257,404 |

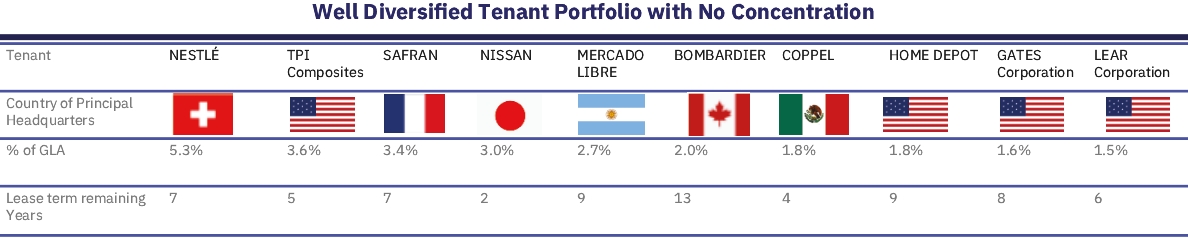

Number of tenants | | | 184 | | | 183 | | | 175 |

Average rent per square foot (US$ per year)(3) | | | 5.3 | | | 5.0 | | | 4.5 |

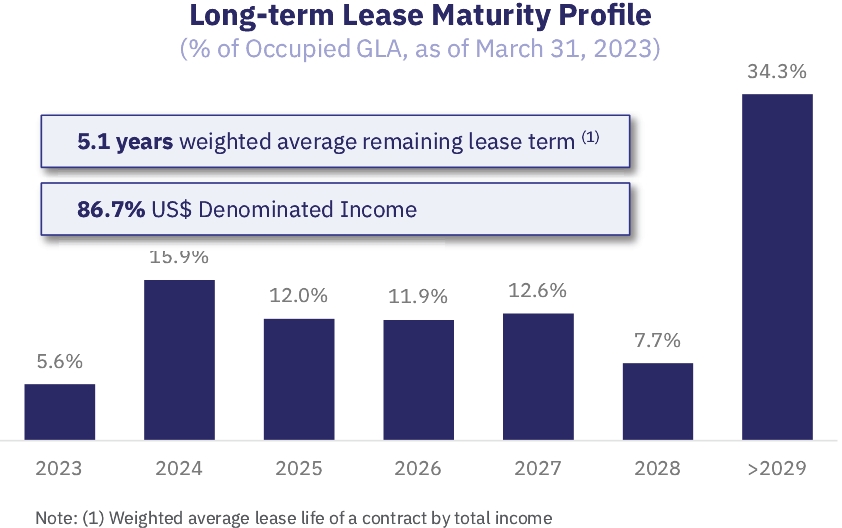

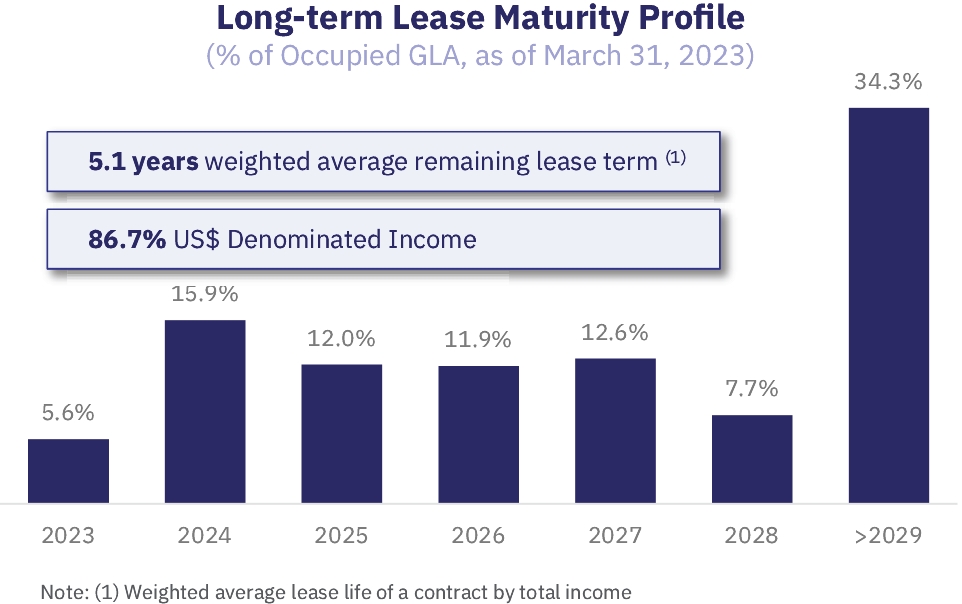

Weighted average remaining lease term (years) | | | 5.1 | | | 4.9 | | | 4.3 |

Collected rental revenues per square foot (US$ per year)(4) | | | 5.3 | | | 4.7 | | | 4.7 |

Stabilized Occupancy rate (% of GLA)(5) | | | 96.7 | | | 97.3 | | | 94.3 |

(1) | Refers to the total GLA across all of our real estate properties. |

(2) | Refers to the GLA that was actually leased to tenants as of the dates indicated. |

(3) | Calculated as the annual base rent as of the end of the relevant period divided by the GLA. For rents denominated in pesos, annual rent is converted to US$ at the average exchange rate for each quarter. |

(4) | Calculated as the annual income collected from rental revenues during the relevant period divided by the square feet leased. For income collected denominated in pesos, income collected is converted to US$ at the average exchange rate for each quarter. |

(5) | We calculate stabilized occupancy rate as leased area divided by total GLA. We deem a property to be stabilized once it has reached 80.0% occupancy or has been completed for more than one year, whichever occurs first. |

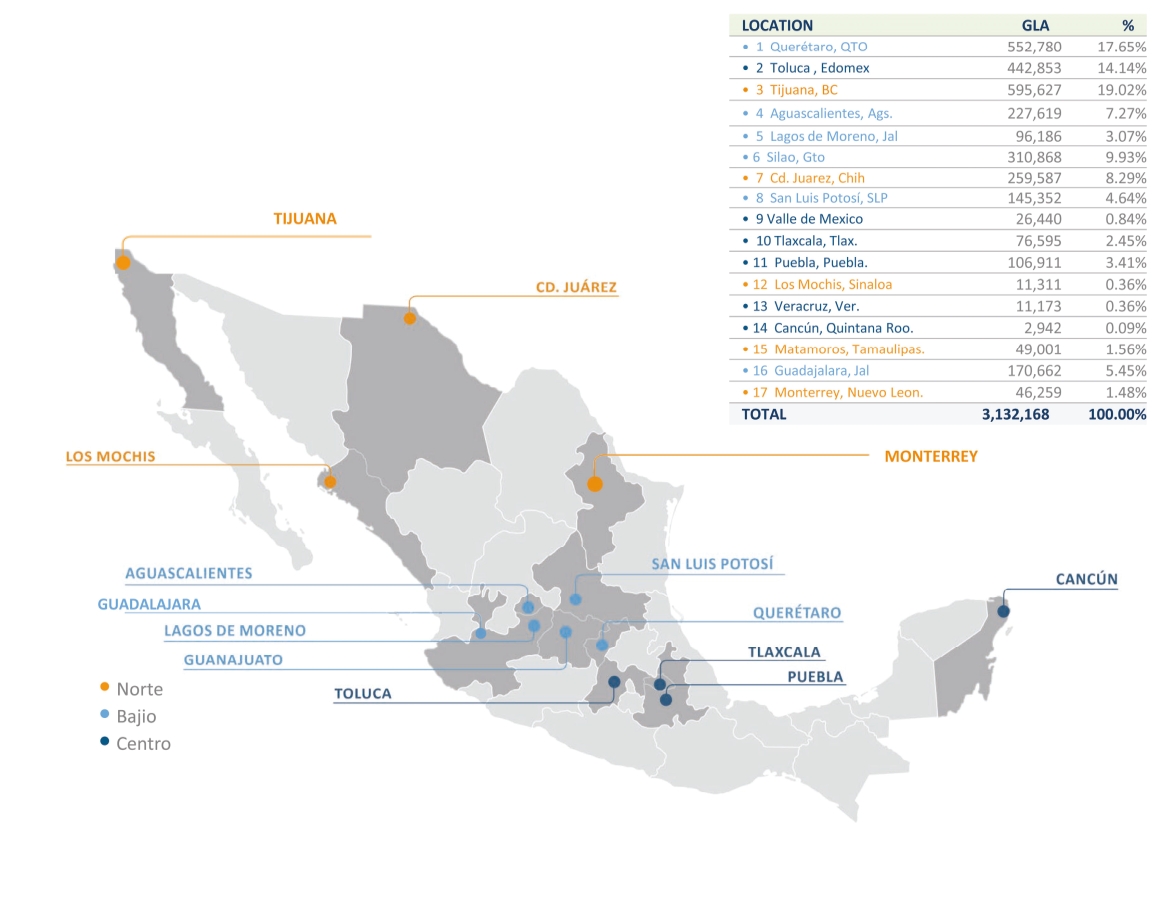

| | | Location | | | Total GLA | | | Total GLA | | | Percentage of Portfolio GLA | | | Rental Income for the Three Months Ended March 31, 2023 | | | Percentage of Rental Income for the Three Months Ended March 31, 2023 | | | Operations Start Year | | | Number of Buildings | | | Appraisal Value as of March 31, 2023 | |

| | | | | (in square feet) | | | (in square meters) | | | (%) | | | (US$) | | | (%) | | | | | | | (US$) | ||||

Industrial Park | | | | | | | | | | | | | | | | | | | |||||||||

DSP | | | Aguascalientes | | | 2,143,262 | | | 199,116 | | | 6.4 | | | 3,141,325 | | | 6.3 | | | 2013 | | | 8 | | | 139,000,000 |

Vesta Park Aguascalientes | | | Aguascalientes | | | 306,804 | | | 28,503 | | | 0.9 | | | 178,034 | | | 0.4 | | | 2019 | | | 2 | | | 17,200,000 |

Los Bravos Vesta Park | | | Cd Juárez | | | 460,477 | | | 42,780 | | | 1.4 | | | 661,584 | | | 1.3 | | | 2007 | | | 4 | | | 29,510,000 |

Vesta Park Juárez Sur I | | | Cd Juárez | | | 1,514,249 | | | 140,678 | | | 4.5 | | | 2,360,859 | | | 4.7 | | | 2015 | | | 8 | | | 110,410,000 |

Vesta Park Guadalajara | | | Guadalajara | | | 1,836,990 | | | 170,662 | | | 5.4 | | | 2,944,562 | | | 5.9 | | | 2020 | | | 4 | | | 158,700,000 |

Vesta Park Guadalupe | | | Monterrey | | | 497,929 | | | 46,259 | | | 1.5 | | | 765,009 | | | 1.5 | | | 2021 | | | 2 | | | 32,800,000 |

Vesta Puebla I | | | Puebla | | | 1,028,564 | | | 95,557 | | | 3.1 | | | 1,651,529 | | | 3.3 | | | 2016 | | | 5 | | | 76,800,000 |

Bernardo Quintana | | | Querétaro | | | 772,025 | | | 71,723 | | | 2.3 | | | 662,821 | | | 1.3 | | | 1998 | | | 9 | | | 38,800,000 |

PIQ | | | Querétaro | | | 1,998,727 | | | 185,688 | | | 5.9 | | | 2,701,433 | | | 5.4 | | | 2006 | | | 13 | | | 128,960,000 |

VP Querétaro | | | Querétaro | | | 923,238 | | | 85,772 | | | 2.7 | | | 684,193 | | | 1.4 | | | 2018 | | | 4 | | | 52,500,000 |

Querétaro Aerospace Park | | | Querétaro Aero | | | 2,256,090 | | | 209,598 | | | 6.7 | | | 3,546,886 | | | 7.1 | | | 2007 | | | 13 | | | 160,600,000 |

SMA | | | San Miguel de Allende | | | 1,361,878 | | | 126,523 | | | 4.0 | | | 1,630,457 | | | 3.2 | | | 2015 | | | 8 | | | 87,300,000 |

Las Colinas | | | Silao | | | 903,487 | | | 83,937 | | | 2.7 | | | 1,184,551 | | | 2.4 | | | 2008 | | | 7 | | | 54,100,000 |

Vesta Park Puento Interior | | | Silao | | | 1,080,795 | | | 100,409 | | | 3.2 | | | 1,321,339 | | | 2.6 | | | 2018 | | | 6 | | | 64,900,000 |

Tres Naciones | | | San Luis Potosí | | | 960,964 | | | 89,276 | | | 2.9 | | | 1,349,647 | | | 2.7 | | | 1999 | | | 9 | | | 59,050,000 |

Vesta Park SLP | | | San Luis Potosí | | | 603,594 | | | 56,076 | | | 1.8 | | | 317,886 | | | 0.6 | | | 2018 | | | 3 | | | 33,700,000 |

La Mesa Vesta Park | | | Tijuana | | | 810,013 | | | 75,253 | | | 2.4 | | | 1,163,790 | | | 2.3 | | | 2005 | | | 16 | | | 62,230,000 |

Nordika | | | Tijuana | | | 469,228 | | | 43,593 | | | 1.4 | | | 634,229 | | | 1.3 | | | 2007 | | | 2 | | | 49,650,000 |

El potrero | | | Tijuana | | | 282,768 | | | 26,270 | | | 0.8 | | | 378,726 | | | 0.8 | | | 2012 | | | 2 | | | 26,550,000 |

Vesta Park Tijuana III | | | Tijuana | | | 620,547 | | | 57,651 | | | 1.8 | | | 985,816 | | | 2.0 | | | 2014 | | | 3 | | | 52,930,000 |

Vesta Park Pacifico | | | Tijuana | | | 379,882 | | | 35,292 | | | 1.1 | | | 590,348 | | | 1.2 | | | 2017 | | | 2 | | | 30,600,000 |

VP Lago Este | | | Tijuana | | | 552,452 | | | 51,324 | | | 1.6 | | | 892,774 | | | 1.8 | | | 2018 | | | 2 | | | 61,500,000 |

Vesta Park Megaregion | | | Tijuana | | | 724,153 | | | 67,276 | | | 2.1 | | | 260,165 | | | 0.5 | | | 2022 | | | 4 | | | 58,640,000 |

VPT I | | | Tlaxcala | | | 680,616 | | | 63,231 | | | 2.0 | | | 1,002,774 | | | 2.0 | | | 2015 | | | 4 | | | 43,500,000 |

Exportec | | | Toluca | | | 220,122 | | | 20,450 | | | 0.7 | | | 275,964 | | | 0.5 | | | 1998 | | | 3 | | | 14,210,000 |

T 2000 | | | Toluca | | | 1,070,180 | | | 99,423 | | | 3.2 | | | 1,505,499 | | | 3.0 | | | 1998 | | | 3 | | | 79,470,000 |

El Coecillo Vesta Park | | | Toluca | | | 816,056 | | | 75,814 | | | 2.4 | | | 1,185,996 | | | 2.4 | | | 2007 | | | 1 | | | 52,210,000 |

Vesta Park Toluca I | | | Toluca | | | 1,000,161 | | | 92,918 | | | 3.0 | | | 1,477,622 | | | 2.9 | | | 2006 | | | 5 | | | 73,480,000 |

Vesta Park Toluca II | | | Toluca | | | 1,473,199 | | | 136,865 | | | 4.4 | | | 2,282,403 | | | 4.5 | | | 2014 | | | 6 | | | 110,800,000 |

Other | | | | | 5,965,921 | | | 554,252 | | | 17.7 | | | 9,237,909 | | | 18.4 | | | na | | | 44 | | | 466,410,000 | |

| | | Total | | | 33,714,370 | | | 3,132,168 | | | 100.0 | | | 46,976,132 | | | 93.6 | | | | | 202 | | | 2,426,510,000 | ||

| | | Other income (reimbursements)(2) | | | 2,890,211 | | | 6.4 | | | | | | | |||||||||||||

| | | Total | | | 49,866,343 | | | 100.0 | | | Vesta Offices at the DSP Park(3) | | | 300,000 | |||||||||||||

| | | | | | | | | | | | | | | Under construction | | | 256,630,000 | ||||||||||

| | | | | | | | | | | | | | | Total | | | 2,683,440,000 | ||||||||||

| | | | | | | | | | | | | | | Land improvements | | | 11,109,593 | ||||||||||

| | | | | | | | | | | | | | | Land Reserves | | | 208,910,000 | ||||||||||

| | | | | | | | | | | | | | | Costs to Complete Construction in Process | | | 111,186,123 | ||||||||||

| | | | | | | | | | | | | | | Appraisal Total | | | 2,792,273,469 | ||||||||||

(1) | Other income (reimbursements) includes: (i) the reimbursement of payments made by us on behalf of some of our tenants to cover maintenance fees and other services, which we incur under the respective lease contracts; and (ii) management fees arising from the real estate portfolio we sold in May 2019. |

(2) | Refers to the appraisal value of our corporate offices located at the Douki Seisan Park. |

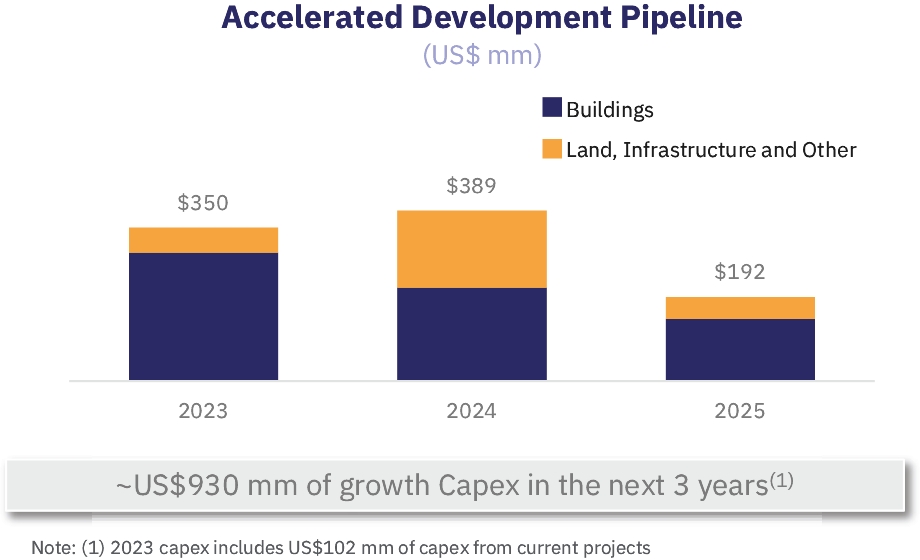

| | | | | | | Total Expected Investment (Thousand US$)(1) | | | Investment to Date (Thousand US$) | | | | | | | ||||||||||||||||||

| | | Project | | | Project GLA | | | Land + Infrastructure | | | Shell(2) | | | Total | | | Land + Infrastructure | | | Shell(2) | | | Total | | | Leased | | | Expected Completion Date | | | Type | |

| | | | | (in square feet) | | | (US$) | | | (US$) | | | (US$) | | | (US$) | | | (US$) | | | (US$) | | | (%) | | | | | ||||

North Region | | | | | | | | | | | | | | | | | | | | | | | |||||||||||

Tijuana | | | Mega Región 05 | | | 359,660 | | | 7,885 | | | 17,387 | | | 25,272 | | | 7,491 | | | 6,955 | | | 14,446 | | | 0.0 | | | July 2023 | | | Inventory |

Tijuana | | | Mega Región 06 | | | 114,725 | | | 2,739 | | | 6,643 | | | 9,382 | | | 2,602 | | | 2,657 | | | 5,260 | | | 0.0 | | | July 2023 | | | Inventory |

Monterrey | | | Apodaca 01 | | | 297,418 | | | 5,201 | | | 9,496 | | | 14,697 | | | 4,941 | | | 7,122 | | | 12,063 | | | 100.0 | | | April 2023 | | | Inventory |

Monterrey | | | Apodaca 02 | | | 279,001 | | | 4,329 | | | 10,175 | | | 14,504 | | | 4,112 | | | 6,614 | | | 10,726 | | | 100.0 | | | September 2023 | | | Inventory |

Monterrey | | | Apodaca 03 | | | 222,942 | | | 5,521 | | | 8,758 | | | 14,279 | | | 5,245 | | | 3,731 | | | 8,976 | | | 0.0 | | | July 2023 | | | Inventory |

Monterrey | | | Apodaca 04 | | | 222,942 | | | 5,544 | | | 8,817 | | | 14,361 | | | 5,267 | | | 3,756 | | | 9,023 | | | 0.0 | | | August 2023 | | | Inventory |

Juárez | | | Juárez Oriente 1 | | | 279,117 | | | 6,539 | | | 11,703 | | | 18,241 | | | 5,231 | | | 5,266 | | | 10,497 | | | 0.0 | | | July 2023 | | | Inventory |

Juárez | | | Juárez Oriente 2 | | | 250,272 | | | 5,492 | | | 10,844 | | | 16,335 | | | 4,393 | | | 4,880 | | | 9,273 | | | 100.0 | | | July 2023 | | | Inventory |

| | | | | 2,026,078 | | | 43,249 | | | 83,824 | | | 127,072 | | | 39,282 | | | 40,981 | | | 80,263 | | | 40.8 | | | | | ||||

Bajío Region | | | | | | | | | | | | | | | | | | | | | | | |||||||||||

Guadalajara | | | GDL 06 | | | 341,969 | | | 7,278 | | | 14,511 | | | 21,790 | | | 6,551 | | | 9,940 | | | 16,491 | | | 0.0 | | | June 2023 | | | Inventory |

Guadalajara | | | GDL 07 | | | 393,938 | | | 8,509 | | | 16,335 | | | 24,843 | | | 7,658 | | | 13,362 | | | 21,020 | | | 100.0 | | | July 2023 | | | Inventory |

Guadalajara | | | GDL 08 | | | 680,333 | | | 15,387 | | | 27,911 | | | 43,297 | | | 13,848 | | | 11,890 | | | 25,738 | | | 0.0 | | | October 2023 | | | Inventory |

Silao | | | Puerto Interior 3 | | | 231,252 | | | 3,445 | | | 9,326 | | | 12,770 | | | 3,445 | | | 4,197 | | | 7,641 | | | 0.0 | | | August 2023 | | | Inventory |

Querétaro | | | Safran Exp | | | 81,158 | | | 0 | | | 4,446 | | | 4,446 | | | 0 | | | 4,135 | | | 4,135 | | | 100.0 | | | May 2023 | | | BTS |

| | | Oxxo Exp | | | 110,764 | | | 1,970 | | | 5,494 | | | 7,465 | | | 1,970 | | | 4,033 | | | 6,003 | | | 100.0 | | | April 2023 | | | BTS | |

| | | | | 1,839,413 | | | 36,589 | | | 78,023 | | | 114,612 | | | 33,471 | | | 47,556 | | | 81,028 | | | 31.9 | | | | | ||||

Total | | | | | 3,865,491 | | | 79,838 | | | 161,846 | | | 241,684 | | | 72,753 | | | 88,537 | | | 161,291 | | | 36.5 | | | | | |||

(1) | Total Expected Investment comprises our material cash requirements, including commitments for capital expenditures. |

(2) | A shell is typically comprised by the primary structure, the building envelope (roof and façade), mechanical and supply systems (electricity, water and drainage) up to a single point of contact. |

Location | | | Total Land Reserves | | | Total Land Reserves | | | Percentage of Total Land Reserves | | | Appraisal Value as of March 31, 2023(1) | | | Estimated GLA to be Developed | | | Estimated GLA to be Developed |

| | | (Hectares) | | | (Acres) | | | (%) | | | (thousands of US$) | | | (square meters) | | | (square feet) | |

Aguascalientes | | | 120 | | | 297 | | | 34 | | | 32,490 | | | 541,304 | | | 5,826,547 |

Querétaro | | | 52 | | | 128 | | | 14.6 | | | 33,680 | | | 232,908 | | | 2,506,997 |

Monterrey | | | 41 | | | 101 | | | 11.5 | | | 32,660 | | | 183,626 | | | 1,976,530 |

San Miguel Allende | | | 36 | | | 89 | | | 10.2 | | | 15,530 | | | 161,801 | | | 1,741,607 |

San Luis Potosí | | | 31 | | | 77 | | | 8.8 | | | 13,320 | | | 140,703 | | | 1,514,511 |

Guanajuato | | | 32 | | | 78 | | | 9.0 | | | 17,720 | | | 142,350 | | | 1,532,242 |

México | | | 24 | | | 60 | | | 6.9 | | | 49,960 | | | 109,899 | | | 1,182,947 |

Ciudad Juárez | | | 16 | | | 40 | | | 4.5 | | | 12,760 | | | 73,587 | | | 792,082 |

Guadalajara | | | 0 | | | 0 | | | 0 | | | 0 | | | 25,504 | | | 274,521 |

Tijuana | | | 0 | | | 0 | | | 0 | | | 0 | | | 22,571 | | | 242,949 |

Puebla | | | 1 | | | 2.1 | | | 0.2 | | | 790 | | | 3,869 | | | 41,647 |

Total | | | 353 | | | 873.1 | | | 100.0 | | | 208,910 | | | 1,590,046 | | | 17,115,108 |

(1) | Land value is appraised at cost. For more information, see “Presentation of Financial and Certain Other Information—Appraisals.” |

• | geopolitical tensions between the U.S. and China leading to relocation of Asia-based operations to North America; |

• | pandemic-disrupted supply chains, including shortages of raw materials and manufacturing components; |

• | a challenging labor and logistics environment in the U.S.; and |

• | the Russia-Ukraine conflict. |

| | |  |

• | Governance and integrity: (i) 100.0% of investment decisions under responsible investment guidelines, including the United Nations Principles for Responsible Investments (“UN PRI”), (ii) establish ESG commitments with 35% of our total supply chain, and (iii) additional women as permanent members of our Board of Directors, consistent with global trends; |

• | Social: (i) achieve strategic alliances for our ESG projects (for example, with local communities and other private organizations), consisting of increasing the total impact of the initiatives, both in terms of people and size of projects, (ii) firm-wide continuous training in ESG practices, and (iii) reduce salary gender gap, primarily at the management level; and |

• | Environment: (i) reduce carbon footprint and water consumption in areas of real estate development managed or to be managed by Vesta, (ii) increase waste recycled by Vesta, (iii) identify all physical and transitional risks of our portfolio and operations to determine mitigation and prevention actions, and (iv) increase the percentage of our GLA to have green certifications, such as LEED, BOMA and EDGE. |

• | The success of our business depends on general economic conditions and prevailing conditions in the real estate industry. Accordingly, any economic slowdown or downturn in real estate asset values or leasing activity may have a material adverse effect on our business, financial condition, results of operations and prospects and/or the liquidity or trading price of our ADSs. |

• | The volatility of the financial markets may adversely affect our financial condition and/or results of operations. |

• | Real estate investments are not as liquid as certain other types of assets, which may adversely affect our financial conditions and results of operations. |

• | Investments in real estate properties are subject to risks that could adversely affect our business. |

• | We are dependent on our tenants for a substantial portion of our revenues and our business would be materially and adversely affected if a significant number of our tenants, or any of our major tenants, were to default on their obligations under their leases. |

• | We derive a significant portion of our rental income from a limited number of customers. |

• | Our clients operate in certain specific industrial sectors in Mexico, and our business may be adversely affected by an economic downturn in any of those sectors. |

• | An increase in competition could lead to lower occupancy rates and rental income and could result in fewer investment opportunities. |

• | We may not be successful in executing on our accelerated growth strategy if we are unable to make acquisitions of land or properties. |

• | We are dependent on our ability to raise capital through financial markets, divestitures or other sources to meet our future growth expectations. |

• | We are subject to risks related to the development of new properties, including due to an increase in construction costs and supply chain issues. |

• | Our business and operations could suffer in the event of system failures or cyber security attacks. |

• | Adverse economic conditions in Mexico may have a negative impact on our financial condition and/or results of operations. |

• | Political and social developments in Mexico as well as changes in Federal Governmental policies could have a negative impact on our business and results of operations. |

• | Legislative or regulatory action with respect to tax laws and regulations could adversely affect us. |

• | Developments in the U.S. and other countries may adversely affect Mexico’s economy, our business, financial condition and/or results of operations, and the market price of our ADSs. |

• | Mexico is an emerging market economy, with risks to our results of operations and financial condition. |

• | Changes in exchange rates between the peso and the U.S. dollar or other currencies may adversely affect our financial condition and/or results of operations. |

• | The price of our ADSs or common shares may be volatile or may decline regardless of our operating performance, and you may not be able to resell your ADSs or common shares at or above the offering price. |

• | Our bylaws contain restrictions on certain transfers of common shares and the execution of shareholders agreements, which could impede the ability of holders of ADSs to benefit from a change in control or to change our management and Board of Directors. |

• | You may not be able to sell your ADSs at the time or the price you desire because an active or liquid market may not develop. |

• | The relative volatility and illiquidity of the Mexican securities markets may substantially limit your ability to sell the common shares underlying the ADSs at the price and time you desire. |

• | Sales of our ADSs or common shares by our founders, directors or officers, or the perception that these sales may occur may cause our share price to decline. |

• | We are subject to different disclosure and accounting standards than companies in other countries. |

• | If we issue or sell additional equity securities in the future, we may suffer dilution and the trading prices for our securities may decline. |

• | The payment and amount of dividends are subject to the determination of our shareholders. |

• | As a foreign private issuer and an “emerging growth company” (as defined in the JOBS Act), we will have different disclosure and other requirements than U.S. registrants and non-emerging growth companies. |

• | We may lose our foreign private issuer status, which would then require us to comply with the Exchange Act’s domestic reporting regime and cause us to incur additional legal, accounting and other expenses. |

• | As a foreign private issuer, we rely on exemptions from certain NYSE corporate governance standards applicable to U.S. issuers, including the requirement that a majority of an issuer’s directors consist of independent directors. This may afford less protection to holders of our common shares. |

• | There can be no assurance that we will not be a passive foreign investment company, or PFIC, for any taxable year, which could result in adverse U.S. federal income tax consequences to U.S. investors in our common shares or our ADSs. |

| | | For the Three-Month Period Ended March 31, | | | For the Year Ended December 31, | |||||||

| | | 2023 | | | 2022 | | | 2022 | | | 2021 | |

| | | (millions of US$, except per share data) | ||||||||||

Revenue: | | | | | | | | | ||||

Rental income | | | 49.9 | | | 42.0 | | | 178.0 | | | 160.7 |

Management fees | | | 0.3 | | | — | | | — | | | 0.1 |

Property operating costs related to properties that generated rental income | | | (2.5) | | | (1.6) | | | (8.9) | | | (8.5) |

Property operating costs related to properties that did not generate rental income | | | (0.7) | | | (0.5) | | | (2.5) | | | (2.2) |

General and administrative expenses | | | (8.2) | | | (6.5) | | | (24.4) | | | (21.4) |

Interest income | | | 0.6 | | | — | | | 2.6 | | | 0.1 |

Other income – net | | | (0.1) | | | — | | | 1.0 | | | — |

Finance costs | | | (11.6) | | | (10.4) | | | (46.4) | | | (50.3) |

Exchange gain (loss) – net | | | 4.6 | | | (0.8) | | | 1.9 | | | (1.1) |

Gain on sale of investment property | | | — | | | 0.6 | | | 5.0 | | | 14.0 |

Gain on revaluation of investment property | | | 10.8 | | | 38.2 | | | 185.5 | | | 164.6 |

Profit before income taxes | | | 43.1 | | | 61.0 | | | 291.8 | | | 256.0 |

Current income tax expense | | | (20.7) | | | (9.1) | | | (42.0) | | | (50.3) |

Deferred income tax | | | 8.5 | | | (2.5) | | | (6.2) | | | (31.8) |

Total income tax benefit (expense) | | | 12.2 | | | (11.6) | | | (48.2) | | | (82.1) |

Profit for the period | | | 30.9 | | | 49.4 | | | 243.6 | | | 173.9 |

Other comprehensive income (loss) – net of tax: | | | | | | | | | | |||

Items that may be reclassified subsequently to profit – Fair value gain on derivative instruments | | | — | | | — | | | — | | | 2.9 |

Exchange differences on translating other functional currency operations | | | 3.8 | | | 5.9 | | | 8.9 | | | (4.8) |

Total other comprehensive loss | | | 3.8 | | | 5.9 | | | 8.9 | | | (2.0) |

Total comprehensive income for the period | | | 34.7 | | | 55.3 | | | 252.5 | | | 172.0 |

Basic earnings per share | | | 0.0452 | | | 0.0718 | | | 0.3569 | | | 0.2683 |

Diluted earnings per share | | | 0.0445 | | | 0.0708 | | | 0.3509 | | | 0.2636 |

| | | As of March 31, | | | As of December 31, | ||||

| | | 2023 | | | 2022 | | | 2021 | |

| | | (millions of US$) | |||||||

Assets | | | | | | | |||

Current assets: | | | | | | | |||

Cash, cash equivalents and restricted cash | | | 98.2 | | | 139.1 | | | 452.8 |

Recoverable taxes | | | 25.7 | | | 30.1 | | | 19.4 |

Operating lease receivables | | | 11.0 | | | 7.7 | | | 9.0 |

Prepaid expenses and advance payments | | | 23.2 | | | 25.3 | | | 0.5 |

Total current assets | | | 158.2 | | | 202.2 | | | 481.7 |

Non-current assets: | | | | | | | |||

Investment property | | | 2,792.3 | | | 2,738.5 | | | 2,263.2 |

Office furniture – Net | | | 1.3 | | | 1.4 | | | 2.1 |

Right-of-use asset | | | 1.3 | | | 1.4 | | | 1.3 |

Guarantee deposits made, restricted cash and others | | | 9.8 | | | 9.6 | | | 11.5 |

Total non-current assets | | | 2,804.7 | | | 2,750.9 | | | 2,278.2 |

Total assets | | | 2,962.9 | | | 2,953.1 | | | 2,759.9 |

| | | | | | | ||||

Liabilities and stockholders’ equity | | | | | | | |||

Current liabilities: | | | | | | | |||

Current portion of long-term debt | | | 4.6 | | | 4.6 | | | 2.9 |

Leases payable – short term | | | 0.7 | | | 0.6 | | | 0.5 |

Accrued interest | | | 7.9 | | | 3.8 | | | 3.8 |

Accounts payable | | | 10.3 | | | 16.6 | | | 3.0 |

Income tax payable | | | 11.9 | | | 14.8 | | | 27.8 |

Accrued expenses and taxes | | | 3.5 | | | 5.2 | | | 15.3 |

Dividends payable | | | 60.3 | | | 14.4 | | | 13.9 |

Total current liabilities | | | 99.1 | | | 60.0 | | | 67.2 |

Non-current liabilities: | | | | | | | |||

Long-term debt | | | 925.0 | | | 925.9 | | | 930.7 |

Leases payable – long term | | | 0.8 | | | 0.9 | | | 0.9 |

Guarantee deposits received | | | 19.9 | | | 18.3 | | | 15.9 |

Long-term account payable | | | 7.8 | | | 7.9 | | | — |

Employee benefits | | | 0.7 | | | 0.3 | | | — |

Deferred income tax | | | 292.6 | | | 300.0 | | | 291.6 |

Total non-current liabilities | | | 1,246.8 | | | 1,253.3 | | | 1,239.0 |

Total liabilities | | | 1,345.9 | | | 1,313.3 | | | 1,306.2 |

Stockholders’ equity: | | | | | | | |||

Capital stock | | | 482.8 | | | 480.6 | | | 482.9 |

Additional paid-in capital | | | 468.7 | | | 460.7 | | | 466.2 |

Retained earnings | | | 704.0 | | | 733.4 | | | 547.2 |

Share-based payments reserve | | | (1.4) | | | 6.0 | | | 7.1 |

Foreign currency translation | | | (37.1) | | | (40.9) | | | (49.8) |

Total stockholders’ equity | | | 1,617.0 | | | 1,639.8 | | | 1,453.6 |

Total liabilities and stockholders’ equity | | | 2,962.9 | | | 2,953.1 | | | 2,759.9 |

| | | For the Three-Month Period Ended March 31, | | | For the Year Ended December 31, | |||||||

| | | 2023 | | | 2022 | | | 2022 | | | 2021 | |

| | | (millions of US$) | ||||||||||

Profit for the period | | | 30.9 | | | 49.4 | | | 243.6 | | | 173.9 |

(+) Total income tax expense | | | 12.2 | | | 11.6 | | | 48.2 | | | 82.1 |

(-) Interest income | | | 0.6 | | | — | | | 2.6 | | | 0.1 |

(-) Other income – net(1) | | | (0.1) | | | — | | | 1.0 | | | — |

(+) Finance costs | | | 11.6 | | | 10.4 | | | 46.4 | | | 50.3 |

(-) Exchange gain (loss) - net | | | 4.6 | | | (0.8) | | | 1.9 | | | 1.1 |

(-) Gain on sale of investment property | | | — | | | 0.6 | | | 5.0 | | | 14.0 |

(-) Gain on revaluation of investment property | | | 10.8 | | | 38.2 | | | 185.5 | | | 164.6 |

(+) Depreciation | | | 0.4 | | | 0.3 | | | 1.5 | | | 1.6 |

(+) Long-term incentive plan and Equity plus | | | 2.8 | | | 1.6 | | | 6.7 | | | 5.6 |

Adjusted EBITDA | | | 42.0 | | | 35.3 | | | 150.4 | | | 133.6 |

(+) General and administrative expenses | | | 8.2 | | | 6.5 | | | 24.4 | | | 21.4 |

(-) Long-term incentive plan and Equity plus | | | 2.8 | | | 1.6 | | | 6.7 | | | 5.6 |

NOI | | | 47.4 | | | 40.2 | | | 168.1 | | | 149.4 |

(+) Property operating costs related to properties that did not generate rental income | | | 0.7 | | | 0.5 | | | 2.5 | | | 2.2 |

Adjusted NOI | | | 48.1 | | | 40.7 | | | 170.6 | | | 151.6 |

(1) | Includes other income and expenses unrelated to our operations, such as reimbursements from insurance proceeds, and sales of office equipment. For more information, see note 15 to our audited consolidated financial statements. |

| | | For the Three-Month Period Ended March 31, | ||||||||||

| | | 2023 | | | 2022 | | | 2023 (per share) | | | 2022 (per share) | |

| | | (millions of US$) | ||||||||||

Profit for the period | | | 30.9 | | | 49.4 | | | 0.0452 | | | 0.0720 |

(-) Gain on sale of investment property | | | — | | | 0.6 | | | 0.0000 | | | 0.0009 |

(-) Gain on revaluation of investment property | | | 10.8 | | | 38.2 | | | 0.0158 | | | 0.0557 |

FFO | | | 20.1 | | | 10.6 | | | 0.0294 | | | 0.0155 |

(-) Exchange gain (loss) – net | | | 4.6 | | | (0.8) | | | 0.0067 | | | (0.0012) |

(-) Other income – net(1) | | | (0.1) | | | — | | | (0.0001) | | | 0.0000 |

(-) Interest income | | | 0.6 | | | — | | | 0.0009 | | | 0.0000 |

(+) Total income tax expense | | | 12.2 | | | 11.6 | | | 0.0178 | | | 0.0169 |

(+) Depreciation | | | 0.4 | | | 0.3 | | | 0.0006 | | | 0.0004 |

(+) Long-term incentive plan and Equity plus | | | 2.8 | | | 1.6 | | | 0.0041 | | | 0.0023 |

Vesta FFO | | | 30.4 | | | 24.9 | | | 0.0444 | | | 0.0363 |

(1) | Includes other income and expenses unrelated to our operations, such as reimbursements from insurance proceeds, and sales of office equipment. For more information, see note 15 to our audited consolidated financial statements. |

| | | For the Year Ended December 31, | ||||||||||

| | | 2022 | | | 2021 | | | 2022 (per share) | | | 2021 (per share) | |

| | | (millions of US$) | ||||||||||

Profit for the period | | | 243.6 | | | 173.9 | | | 0.3568 | | | 0.2682 |

(-) Gain on sale of investment property | | | 5.0 | | | 14.0 | | | 0.0073 | | | 0.0216 |

(-) Gain on revaluation of investment property | | | 185.5 | | | 164.6 | | | 0.2717 | | | 0.2538 |

FFO | | | 53.1 | | | (4.7) | | | 0.0778 | | | (0.0072) |

(-) Exchange gain (loss) – net | | | 1.9 | | | (1.1) | | | 0.0028 | | | (0.0017) |

(-) Other income – net(1) | | | 1.0 | | | — | | | 0.0015 | | | 0.0000 |

(-) Interest income | | | 2.6 | | | 0.1 | | | 0.0038 | | | 0.0002 |

(+) Total income tax expense | | | 48.2 | | | 82.1 | | | 0.0706 | | | 0.1266 |

(+) Depreciation | | | 1.5 | | | 1.6 | | | 0.0022 | | | 0.0025 |

(+) Long-term incentive plan and Equity plus | | | 6.7 | | | 5.6 | | | 0.0098 | | | 0.0086 |

Vesta FFO | | | 104.0 | | | 85.6 | | | 0.1523 | | | 0.1320 |

(1) | Includes other income and expenses unrelated to our operations, such as reimbursements from insurance proceeds, and sales of office equipment. For more information, see note 16 to our financial statements. |

| | | As of March 31, | | | As of December 31, | ||||

| | | 2023 | | | 2022 | | | 2021 | |

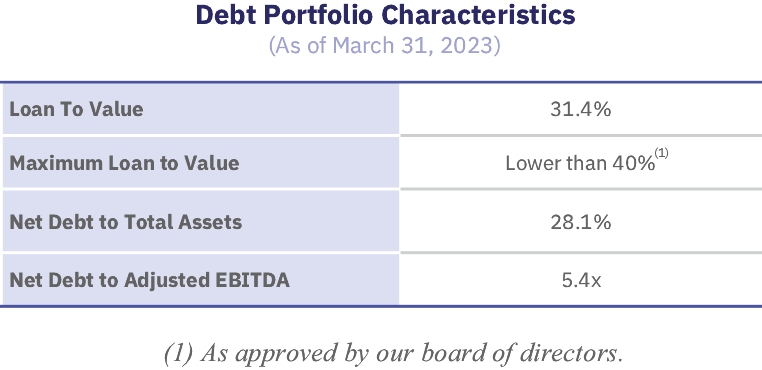

Net Debt to Total Assets(1) | | | 0.3x | | | 0.3x | | | 0.2x |

Net Debt to Adjusted EBITDA(2) | | | 5.4x(3) | | | 5.3x | | | 3.7x |

(1) | Net Debt to Total Assets represents (i) our gross debt (defined as current portion of long-term debt plus long-term debt plus amortization of debt issuance costs) less cash and cash equivalents divided by (ii) total assets. Our management believes that this ratio is useful because it shows the degree in which net debt has been used to finance our assets and using this measure investors and analysts can compare the leverage shown by this ratio with that of other companies in the same industry. |

(2) | Net Debt to Adjusted EBITDA represents (i) our gross debt (defined as current portion of long-term debt plus long-term debt plus amortization of debt issuance costs) less cash and cash equivalents divided by (ii) Adjusted EBITDA. Our management believes that this ratio is useful because it provides investors with information on our ability to repay debt, compared to our performance as measured using Adjusted EBITDA. |

(3) | Net Debt to Adjusted EBITDA as of March 31, 2023, is presented using Adjusted EBITDA as calculated based on a last twelve-months basis, which we calculate as Adjusted EBITDA for the three month period ended March 31, 2023, plus Adjusted EBITDA for the year ended December 31, 2022, less Adjusted EBITDA for the three month period ended March 31, 2022. |

| | | As of March 31, | | | As of December 31, | ||||

| | | 2023 | | | 2022 | | | 2021 | |

| | | (in millions of US$) | |||||||

Total debt | | | 939.4 | | | 940.6 | | | 943.5 |

Current portion of long-term debt | | | 4.6 | | | 4.6 | | | 2.9 |

Long-term debt | | | 925.0 | | | 925.9 | | | 930.7 |

Direct issuance cost | | | 9.8 | | | 10.1 | | | 10.0 |

(-) Cash and cash equivalents | | | 98.2 | | | 139.1 | | | 452.8 |

Net debt | | | 841.2 | | | 801.5 | | | 490.8 |

| | | As of March 31, | | | As of December 31, | ||||

| | | 2023 | | | 2022 | | | 2021 | |

| | | (number of properties) | |||||||

Total properties | | | 202 | | | 202 | | | 189 |

Same-Store Properties | | | 189 | | | 189 | | | 185 |

Non-Same-Store Properties | | | 13 | | | 13 | | | 4 |

| | | As of March 31, | | | As of December 31, | ||||

| | | 2023 | | | 2022 | | | 2021 | |

| | | (millions of US$) | |||||||

Profit for the period | | | 30.9 | | | 243.6 | | | 173.9 |

(+) Total income tax expense | | | 12.2 | | | 48.2 | | | 82.1 |

(-) Interest income | | | 0.6 | | | 2.6 | | | 0.1 |

(-) Other income – net(1) | | | (0.1) | | | 1.0 | | | — |

(+) Finance costs | | | 11.6 | | | 46.4 | | | 50.3 |

(-) Exchange gain (loss) - net | | | 4.6 | | | 1.9 | | | (1.1) |

(-) Gain on sale of investment property | | | — | | | 5.0 | | | 14.0 |

(-) Gain on revaluation of investment property | | | 10.8 | | | 185.5 | | | 164.6 |

(+) General and administrative expenses | | | 8.2 | | | 24.4 | | | 21.4 |

(+) Property operating costs related to properties that did not generate rental income | | | 0.7 | | | 2.5 | | | 2.2 |

(+) Property operating costs related to properties that did generate rental income related to non-Same-Store Properties | | | 0.2 | | | 0.1 | | | 0.6 |

(-) Management fees related to non Same-Store Properties | | | 0.3 | | | — | | | 0.1 |

(-) Rental income related to non Same-Store Properties | | | 5.5 | | | 12.4 | | | 7.7 |

Same-Store NOI | | | 42.1 | | | 156.8 | | | 145.1 |

(1) | Includes other income and expenses unrelated to our operations, such as reimbursements from insurance proceeds, and sales of office equipment. For more information, see note 15 to our audited consolidated financial statements. |

| | | As of March 31, | | | As of December 31, | ||||

| | | 2023 | | | 2022 | | | 2021 | |

Total GLA (sq. feet) | | | 33,714,370 | | | 33,714,370 | | | 31,081,749 |

Total GLA (sq. meters) | | | 3,132,168 | | | 3,132,168 | | | 2,887,589 |

Stabilized occupancy rate(1) | | | 96.7% | | | 97.3% | | | 94.3% |

(1) | Stabilized occupancy rate refers to the rate of occupied stabilized properties only. We deem a property to be stabilized once it has reached 80.0% occupancy or has been completed for more than one year, whichever occurs first. |

• | a general decline in the price of rents or less favorable terms for new leases or renewals; |

• | the depreciation of the value of the properties in our portfolio; |

• | increased vacancy rates or our inability to lease our properties on favorable conditions; |

• | our inability to collect rents from our tenants; |

• | reduced levels of demand for industrial space and industrial facilities, or changes in consumer preferences vis-à-vis our available properties; |

• | an increased supply of industrial facilities or more suitable spaces in the markets in which we operate; |

• | higher interest rates, increased leasing costs, increased construction costs, distressed supply chains for construction materials, increased maintenance costs, reduced availability of financing on favorable terms and shortage of mortgage loans, lines of credit and other capital resources, all of which could increase our costs and limit our ability to acquire or develop additional real estate assets or refinance our debt; |

• | measures that limit our ability to develop acquired land pursuant to existing plans; |

• | increased costs and expenses, including, among other things, for insurance, labor, energy, real estate appraisals, real estate taxes and compliance with applicable laws and regulations; and |

• | the adoption of restrictive government policies or the imposition of limitations on our ability to pass on costs to our customers. |

• | local conditions, such as oversupply or a reduction in demand; |

• | technological changes, such as reconfiguration of supply chains, robotics, 3D printing or other technologies; |

• | the attractiveness and quality of our properties, and related services, to potential tenants and competition from other available properties; |

• | increasing costs of maintaining, insuring, renovating and making improvements to our properties; |

• | our ability to reposition our properties due to changes in the business and logistics needs of our customers; |

• | our ability to lease properties at favorable rates, including periodic increases based on inflation or exchange rates, and control variable operating costs; |

• | social problems, including safety, affecting certain regions; |

• | governmental and environmental regulations and the associated potential liability under, and changes in, environmental, community rights, zoning, usage, tax, tariffs and other laws; and |

• | reduction on the supply, price increases and other restrictions affecting the supply of key resources, such as water and electricity, may affect the construction industry and the operation of rental facilities in Mexico. |

• | we may not be able to acquire desired properties, including other real estate developers and real estate investment funds, particularly in markets in which we do not currently operate; |

• | we may need additional land bank to accelerate our portfolio growth and execute our growth strategy to meet our goals; |

• | we may not be able to obtain financing for the relevant acquisition given our existing leverage position and increased interest rates; |

• | the properties we acquire may not prove accretive to our results, or that we may not be able to successfully manage and lease those properties to meet our goals; |

• | we may not be able to generate sufficient operating cash flows to make an acquisition; |

• | we may need to spend additional amounts than budgeted to develop a property or make necessary improvements or renovations; |

• | competition from other potential acquirors may significantly increase the purchase price of a desired property; |

• | we may spend significant time and money on potential acquisitions that we are unable to make as a result of the lack of satisfaction of customary closing conditions included in the agreements for the acquisition of properties, including the satisfactory completion of due diligence investigations; |

• | we may not be able to obtain any or all regulatory approvals necessary to complete the acquisition, including from the Mexican Antitrust Commission (Comisión Federal de Competencia Economica or “COFECE”); |

• | the process of pursuing and consummating an acquisition may distract the attention of our senior management from our existing business operations; |

• | we may experience delays (temporary or permanent) if there is public or government opposition to our activities; and |

• | we may not be able to rapidly and efficiently integrate new acquisitions, especially acquisitions of real estate portfolios, to our existing operations. |

• | shortages of materials or skilled labor; |

• | a change in the scope of the original project; |

• | the difficulty in obtaining necessary zoning, land-use, environmental, health & safety, building, occupancy, antitrust and other governmental permits; |

• | economic or political conditions affecting the relevant location; |

• | an increase in the cost of building materials and equipment; |

• | the discovery of structural or other latent defects in the property once construction has commenced; and |

• | delays in securing tenants. |

• | the appetite of investors; |

• | our financial performance and that of our tenants; |

• | our ability to meet market expectations and the expectations of our investors with respect to our business; |

• | the reports of financial analysts with respect to our business; |

• | the prevailing economic, political and social environment in Mexico; |

• | the condition of the capital markets, including changes in the prevailing interest rates for fixed-income securities; |

• | the prevailing legal environment in Mexico with respect to the protection of minority shareholder interests; |

• | distributions to our shareholders, which largely depend on our operating cash flows, which in turn are dependent on the increase of revenues from our developments and acquisitions, the increase of our rental income, and on committed projects and capital expenditures; and |

• | other factors, such as changes in regulation (including, in particular, any changes in tax, labor and environmental regulation) or the adoption of other governmental or legislative measures affecting the real estate industry generally or us particularly. |

• | incur additional indebtedness; |

• | repay our debts prior to their stated maturities; |

• | make acquisitions or investments or take advantage of business opportunities; |

• | create or incur additional liens; |

• | divest assets when they are subject to collateral restrictions; |

• | transfer or sell certain assets or merge or consolidate with other entities; |

• | implement mergers, spin-offs or business reorganizations of our business; |

• | enter into certain transactions with affiliates; |

• | sell shares in our subsidiaries and/or enter into joint ventures; and |

• | take certain other corporate actions that would otherwise be desirable. |

• | we may not be able to lease space in our new properties at profitable prices; |

• | we may abandon development opportunities and fail to capitalize on our investments in research and valuation in connection with those opportunities; |

• | we may not be able to obtain or may experience delays in obtaining all of the requisite zoning, building, occupancy and other governmental permits and authorizations; |

• | the feasibility studies for the development of new properties may prove incorrect once the development has commenced; |

• | our business activities may not be as profitable as expected as a result of increased costs of Land Reserves; |

• | actual costs of construction of a project may exceed our original estimates or the construction may not be completed on schedule, for example, as a result of delays attributable to contractual defaults, local climate conditions, nationwide or local strikes by construction workers or shortages of construction materials or electric power or fuel for our equipment, any of which would render the project less profitable or unprofitable; |

• | we may be forced to incur additional costs to correct defects in construction design or that are demanded by our tenants; and |

• | we may be held jointly liable for any underlying soil contamination on any of our properties with the party that caused that contamination, even if that contamination was not identifiable by us. |

• | working to formalize internal control processes and documentation; |

• | working to strengthen supervisory reviews by our management in charge of financial issues; |

• | working to hire additional qualified accounting and finance personnel and to engage financial consultants to enable the implementation of internal control over financial reporting and to segregate duties amongst our accounting and finance personnel; |

• | planning to improve our accounting systems to automate manual processes; and |

• | engaging third parties as required to assist with technical accounting, application of new accounting standards, tax matters, valuations of investment properties, and ESG sustainability metrics, among other matters. |

• | general and industry-specific economic conditions; |

• | differences between our actual financial and operating results and those expected by investors; |

• | investors’ perceptions of our prospects and the prospects of the industries in which we operate; |

• | our financial performance and changes in financial estimates or recommendations by securities analysts or failure to meet analysts’ performance expectations; |

• | the occurrence of health threats; |

• | new conflicts or the escalation of existing conflicts around the world; |

• | new laws or regulations or new interpretations of existing laws and regulations, including tax guidelines, environmental matters and regulation on investment applicable to the real estate industry and our business and our common shares and ADSs; |

• | regulatory developments affecting us or our industry; |

• | new accounting policies and pronouncements; |

• | general economic trends in the U.S., Latin American or global economies and financial markets, including those resulting from war, terrorist attacks or responses to those events; |

• | changes in earnings projections or in research reports about us or the Mexican real-estate industry; |

• | security issues in Mexico; |

• | litigation and insolvency proceedings involving Mexican public companies; |

• | measures and guidelines relating to the protection of minority investors in Mexican companies; |

• | liquidity affecting the Mexican stock markets; |

• | media and public speculation; |

• | changes in sovereign ratings or outlooks of Latin American countries, particularly Mexico, or changes in our ratings or outlook or those of other real estate companies; |

• | political conditions or developments in Mexico, the United States and elsewhere; |

• | additions or departures of key members of management; and |

• | any increased indebtedness we may incur in the future. |

• | it is not satisfied with our controls; |

• | it disagrees with our internal control’s documentation, design, operation or review process; or |

• | its interpretation about relevant requirements is different than ours. |

• | any action between us and our shareholders; and |

• | any action between two or more shareholders or groups of shareholders regarding any matters relating to us. |

• | as an ADS holder, we will not treat you as one of our direct shareholders and you may not be able to exercise shareholder rights; |

• | distributions on the common shares represented by your ADSs will be paid to the depositary, and before the depositary makes a distribution to you on behalf of your ADSs, withholding taxes, if any, that must be paid will be deducted and the depositary will be required to convert the pesos received into U.S. dollars. Additionally, if the exchange rate fluctuates significantly during a time when the depositary cannot convert the pesos received into U.S. dollars, or while it holds the pesos, you may lose some or all of the U.S. dollar value of the distribution; |

• | we and the depositary may amend or terminate the deposit agreement without the ADS holders’ consent in a manner that could prejudice the holders of ADSs or that could affect the ability of the holders of ADSs to transfer ADSs; and |

• | the depositary may take other actions inconsistent with the best interests of the holders of ADSs. |

• | from earnings included in year-end audited consolidated financial statements that are approved by shareholders at a duly convened meeting (including retained earnings); |

• | after any existing losses applicable to prior years have been made up or absorbed into shareholders’ equity; |

• | after at least 5% of net profits for the relevant fiscal year have been allocated to a legal reserve, until the amount of the reserve equals 20.0% of a company’s paid-in capital stock; |

• | any other reserves have been created, including a reserve for the repurchase of our own common shares; and |

• | after shareholders have approved the payment of the relevant dividends at a duly convened meeting. |

• | more than 50.0% of the voting power of all our outstanding classes of voting securities (on a combined basis) must be either directly or indirectly owned of record by non-residents of the United States; or |

• | (1) a majority of our executive officers or directors must not be U.S. citizens or residents; (2) more than 50.0% of our assets cannot be located in the United States; and (3) our business must be administered principally outside the United States. |

| | | As of March 31, 2023 | ||||

| | | Actual | | | As Adjusted | |

| | | (millions of US$) | ||||

Cash, cash equivalents and restricted cash | | | 98.2 | | | |

Debt: | | | | | ||

Current portion of long-term debt | | | 4.6 | | | |

Long-term debt | | | 925.0 | | | |

Total debt | | | 929.6 | | | |

Stockholders’ equity: | | | | | ||

Capital stock | | | 482.8 | | | |

Additional paid-in capital | | | 468.7 | | | |

Retained earnings | | | 704.0 | | | |

Share-based payments reserve | | | 1.4 | | | |

Foreign currency translation | | | 37.1 | | | |

Valuation of derivative financial instruments | | | — | | | |

Total stockholders’ equity | | | 1,617.0 | | | |

Total capitalization | | | 2,444.8 | | | |

Assumed initial public offering price per common share | | | US$ |

Pro forma net tangible book value per common share as of March 31, 2023 | | | US$ |

Increase in pro forma net tangible book value per common share attributable to existing investor | | | US$ |

Pro forma as adjusted net tangible book value per common share immediately after this offering | | | US$ |

Dilution in pro forma net tangible book value per common share to new investors in this offering | | | US$ |

| | | Common Shares Purchased | | | Total Consideration | | | Average Price Per Common Share | |||||||

| | | Number | | | Percent | | | Amount | | | Percentage | | |||

Existing shareholders | | | | | | | US$ | | | | | US$ | |||

New investors | | | | | | | | | | | | | US$ | ||

Total | | | | | | 100 | | | US$ | | | 100 | | | US$ |

| | | Price | | | Average Trading Volume(1) | |||||||

Period | | | Maximum | | | Minimum | | | Closing | | ||

| | | (in pesos) | | |||||||||

Monthly | | | | | | | | | ||||

January 2022 | | | 41.5 | | | 36.7 | | | 38.4 | | | 1,264,459 |

February 2022 | | | 39.5 | | | 35.2 | | | 38.0 | | | 1,037,187 |

March 2022 | | | 39.4 | | | 36.2 | | | 37.5 | | | 2,502,449 |

April 2022 | | | 39.0 | | | 34.8 | | | 37.2 | | | 1,148,219 |

May 2022 | | | 40.5 | | | 36.2 | | | 37.9 | | | 1,666,223 |

June 2022 | | | 40.1 | | | 35.1 | | | 37.6 | | | 1,554,756 |

July 2022 | | | 41.1 | | | 36.7 | | | 39.5 | | | 1,825,001 |

August 2022 | | | 40.8 | | | 36.8 | | | 38.6 | | | 1,404,714 |

September 2022 | | | 40.1 | | | 36.6 | | | 38.1 | | | 1,612,224 |

October 2022 | | | 44.3 | | | 36.8 | | | 39.3 | | | 1,264,459 |

November 2022 | | | 44.5 | | | 41.6 | | | 43.0 | | | 1,037,187 |

December 2022 | | | 47.6 | | | 43.2 | | | 45.7 | | | 2,502,449 |

January 2023 | | | 52.3 | | | 45.4 | | | 49.0 | | | 1,869,351 |

February 2023 | | | 55.6 | | | 51.2 | | | 53.0 | | | 2,996,167 |

March 2023 | | | 52.3 | | | 50.9 | | | 54.0 | | | 3,104,948 |

April 2023 | | | 55.6 | | | 52.4 | | | 55.0 | | | 2,018,372 |

May 2023 | | | 57.3 | | | 52.5 | | | 55.7 | | | 1,722,844 |

June 2023 (thorugh June 7, 2023) | | | 58.9 | | | 55.3 | | | 57.6 | | | 1,871,289 |

Quarterly | | | | | | | | | ||||

1Q 2022 | | | 41.5 | | | 35.2 | | | 37.9 | | | 1,638,339 |

2Q 2022 | | | 40.5 | | | 34.8 | | | 37.6 | | | 1,461,141 |

3Q 2022 | | | 41.1 | | | 36.6 | | | 38.7 | | | 1,607,612 |

4Q 2022 | | | 47.6 | | | 36.8 | | | 42.7 | | | 2,746,059 |

1Q 2023 | | | 57.1 | | | 45.4 | | | 52.0 | | | 2,785,302 |

| | | Price | | | Average Trading Volume(1) | |||||||

Period | | | Maximum | | | Minimum | | | Closing | | ||

| | | (in pesos) | | |||||||||

Annual | | | | | | | | | ||||

2020 | | | 40.6 | | | 23.5 | | | 33.4 | | | 1,599,808 |

2021 | | | 45.6 | | | 34.3 | | | 38.9 | | | 1,290,927 |

2022 | | | 47.6 | | | 34.8 | | | 39.2 | | | 1,863,169 |

(1) | Volume = Average of daily volume taking into account only the annual period. |

• | an annual report for the immediately preceding fiscal year prepared in accordance with the CNBV’s general regulations by no later than April 30 of each year; |

• | quarterly reports, within 20 business days following the end of each of the first three quarters and 40 business days following the end of the fourth quarter; |

• | reports disclosing material events promptly upon their occurrence; |

• | reports regarding corporate restructurings, such as mergers, acquisitions, spin-offs or asset sales approved at shareholders’ meetings or by the board of directors; |

• | a summary of the resolutions adopted at any shareholders’ meeting, on the business day immediately following the date of that meeting; and |

• | disclosure in respect of certain material agreements among shareholders. |

• | the issuer maintains adequate confidentiality measures (including maintaining records of persons or entities in possession of material non-public information); |

• | the information is related to transactions that have not been completed; |

• | there is no misleading public information relating to the material event; and |

• | no unusual price or volume fluctuation occurs. |

• | if the issuer does not disclose a material event or to comply with reporting obligations; |

• | upon price or volume volatility or changes in the offer or demand for those shares that are not consistent with their historic performance and cannot be explained solely through information made publicly available pursuant to the CNBV’s general regulations; |

• | to prevent disorderly market conditions; or |

• | technological contingencies in the operational systems of the BMV. |

• | members and the secretary of a public entity’s board of directors, its statutory auditor, the chief executive officer and other officers, as well as the external auditors; |

• | any person that, directly or indirectly, controls 10.0% or more of a listed issuer’s outstanding share capital; |

• | members and the secretary of the board of directors, the statutory auditor, the chief executive officer and other officers of companies that, directly or indirectly, control 10.0% or more of a listed issuer’s outstanding share capital; |

• | any person or group of persons who have a significant influence over the issuer and, if applicable, in the companies of the business group or consortium to which the issuer belongs; and |

• | any person who carries out transactions with securities that deviate from their historical investment patterns in the market and who may reasonably have had access to privileged information through the persons referred to in the preceding sections. |

Period | | | Spread | | | Share of Trading Volume |

January 2022 | | | 98,203 | | | 0.23% |

February 2022 | | | 93,211 | | | 0.24% |

March 2022 | | | 144,371 | | | 0.19% |

April 2022 | | | 115,510 | | | 0.22% |

May 2022 | | | 103,433 | | | 0.24% |

June 2022 | | | 162,069 | | | 0.22% |

July 2022 | | | 120,209 | | | 0.20% |

August 2022 | | | 119,454 | | | 0.17% |

September 2022 | | | 122,765 | | | 0.16% |

October 2022 | | | 101,773 | | | 0.12% |

November 2022 | | | 111,781 | | | 0.12% |

December 2022 | | | 137,402 | | | 0.13% |

Average | | | 119,182 | | | 0.12% |

January 2023 | | | 126,227 | | | 6.77% |

February 2023 | | | 125,691 | | | 4.57% |

March 2023 | | | 149,333 | | | 4.43% |

April 2023 | | | 131,024 | | | 4.42% |

May 2023 | | | 152,250 | | | 4.01% |

Average | | | 136,905 | | | 4.84% |

| | | As of March 31, | | | As of December 31, | ||||

| | | 2023 | | | 2022 | | | 2021 | |

Number of real estate properties | | | 202 | | | 202 | | | 189 |

GLA (sq. feet)(1) | | | 33,714,370 | | | 33,714,370 | | | 31,081,746 |

Leased area (sq. feet)(2) | | | 32,064,157 | | | 32,054,026 | | | 29,257,404 |

Number of tenants | | | 184 | | | 183 | | | 175 |

Average rent per square foot (US$ per year)(3) | | | 5.3 | | | 5.0 | | | 4.5 |

Weighted average remaining lease term (years) | | | 5.1 | | | 4.9 | | | 4.3 |

Collected rental revenues per square foot (US$ per year)(4) | | | 5.3 | | | 4.7 | | | 4.7 |

Stabilized Occupancy rate (% of GLA)(5) | | | 96.7 | | | 97.3 | | | 94.3 |

(1) | Refers to the total GLA across all of our real estate properties. |

(2) | Refers to the GLA that was actually leased to tenants as of the dates indicated. |

(3) | Calculated as the annual base rent as of the end of the relevant period divided by the GLA. For rents denominated in pesos, annual rent is converted to US$ at the average exchange rate for each quarter. |

(4) | Calculated as the annual income collected from rental revenues during the relevant period divided by the square feet leased. For income collected denominated in pesos, income collected is converted to US$ at the average exchange rate for each quarter. |

(5) | We calculate stabilized occupancy rate as leased area divided by total GLA. We deem a property to be stabilized once it has reached 80.0% occupancy or has been completed for more than one year, whichever occurs first. |

• | Level 1 fair value measurements are those derived from quoted prices (unadjusted) in active markets for identical assets or liabilities that we can access at the measurement date; |

• | Level 2 fair value measurements are those derived from inputs, other than quoted prices included within Level 1, that are observable for the asset or liability, either directly or indirectly; and |

• | Level 3 fair value measurements are those derived from valuation techniques that include inputs for the asset or liability that are not based on observable market data. |

• | interest income: interest income consists of interest earned on our cash and cash equivalents; |

• | other income: other income includes (i) nonrecurring items related to acquisitions of shares of other companies, and (ii) other miscellaneous items such as inflation and interest on recoverable income taxes; |

• | finance cost: interest expense primarily includes accrued interest on our debt and other financing-related expenses; |

• | exchange gain: based on the primary economic environment in which we operate, our management has determined that the U.S. dollar is the functional currency of Vesta and all of its subsidiaries except for WTN, which considers the peso to be its functional currency. Therefore, exchange gain represents the effect of changes in exchange rates on monetary assets and liabilities denominated in pesos held by Vesta and all of its subsidiaries except for WTN. It also includes the effects of changes in exchange rates on U.S. dollar-denominated indebtedness of WTN. We recognize an exchange gain or loss depending on whether we hold monetary assets or liabilities denominated in pesos and whether the peso appreciates or depreciates against the U.S. dollar; and |

• | gain on revaluation of investment property: gain on revaluation of investment property is the gain derived as a result of changes in the fair value of our investment properties as determined by independent appraisers. The appraisals are performed on a quarterly basis. We record a gain on revaluation of investment property for years in which the fair value of our properties increases as compared to the previous year, or a loss on revaluation of investment property if the fair value decreases. |

| | | For the Three-Month Period Ended March 31, | | | For the Year Ended December 31, | |||||||

| | | 2023 | | | 2022 | | | 2022 | | | 2021 | |

| | | (millions of US$, except per share data) | ||||||||||

Revenues: | | | | | | | | | ||||

Rental income | | | 49.9 | | | 42.0 | | | 178.0 | | | 160.7 |

Management fees | | | 0.3 | | | — | | | — | | | 0.1 |

Property operating costs related to properties that generated rental income | | | (2.5) | | | (1.6) | | | (8.9) | | | (8.5) |

Property operating costs related to properties that did not generate rental income | | | (0.7) | | | (0.5) | | | (2.5) | | | (2.2) |

General and administrative expenses | | | (8.2) | | | (6.5) | | | (24.4) | | | (21.4) |

Interest income | | | 0.6 | | | — | | | 2.6 | | | 0.1 |

Other income – net | | | (0.1) | | | — | | | 1.0 | | | — |

Finance costs | | | (11.6) | | | (10.4) | | | (46.4) | | | (50.3) |

Exchange gain (loss) – net | | | 4.6 | | | (0.8) | | | 1.9 | | | (1.1) |

Gain on sale of investment property | | | — | | | 0.6 | | | 5.0 | | | 14.0 |

Gain on revaluation of investment property | | | 10.8 | | | 38.2 | | | 185.5 | | | 164.6 |

Profit before income taxes | | | 43.1 | | | 61.0 | | | 291.8 | | | 256.0 |

Current income tax expense | | | (20.7) | | | (9.1) | | | (42.0) | | | (50.3) |

Deferred income tax | | | 8.5 | | | (2.5) | | | (6.2) | | | (31.8) |

Total income tax expense | | | (12.2) | | | (11.6) | | | (48.2) | | | (82.1) |

Profit for the period | | | 30.9 | | | 49.4 | | | 243.6 | | | 173.9 |

Other comprehensive income (loss) – net of tax: | | | | | | | | | ||||

Items that may be reclassified subsequently to profit – Fair value gains on derivative instruments | | | — | | | — | | | — | | | 2.9 |

Exchange differences on translating other functional currency operations | | | 3.8 | | | 5.9 | | | 8.9 | | | (4.8) |

Total other comprehensive income (loss) | | | 3.8 | | | 5.9 | | | 8.9 | | | (2.0) |

Total comprehensive income for the period | | | 34.7 | | | 55.3 | | | 252.5 | | | 172.0 |

Basic earnings per share | | | 0.0452 | | | 0.0718 | | | 0.3569 | | | 0.2683 |

Diluted earnings per share | | | 0.0445 | | | 0.0708 | | | 0.3509 | | | 0.2636 |

• | an increase of US$6.1 million, or 14.5%, in rental income from the leasing of new spaces or spaces that were vacant during the first quarter of 2022; |

• | an increase of US$2.3 million, or 5.6%, in rental income resulting from increases on rent per adjustments for inflation in accordance with our leases; |

• | an increase of US$ 0.5 million, or 1.2%, due to the currency translation effects of leases denominated in Mexican pesos; and |

• | an increase of US$0.7 million, or 1.8%, resulting from the reimbursement of expenses paid by us on behalf of our customers and accounted for under rental income. |

• | a decrease of US$1.7 million, or 4.1%, in rental income from leases that expired and were not renewed during the first quarter of 2023; and |

• | a decrease of US$0.1 million, or 0.2%, in rental income as a result of rental rate reductions agreed upon renewal of our leases in order to retain customers. |

• | an increase of US$19.4 million, or 12.0%, in rental income from the leasing of new spaces or spaces that were vacant during 2021; |

• | an increase of US$8.7 million, or 5.4%, in rental income resulting from increases on rent from adjustments for inflation in accordance with our leases; |

• | an increase US$2.7 million, or 40.6%, resulting from the reimbursement of expenses paid by us on behalf of our customers and accounted for under rental income; and |

• | an increase of US$0.3 million, or 0.2%, due to the currency translation effects of leases denominated in Mexican pesos. |

• | a decrease of US$7.8 million in lost lease revenue from properties sold during 2021; |

• | a decrease of US$5.6 million, or 3.5%, in rental income from leases that expired during 2021 and were not renewed for 2022; and |

• | a decrease of US$0.3 million, or 0.2%, in rental income as a result of rental rate reductions agreed upon renewal of our leases in order to retain customers. |

• | a decrease of US$0.1 million, or 3.0%, in real estate taxes due to higher prompt payment discounts in 2022, to US$1.8 million for 2022 from US$1.9 million for 2021; |

• | an increase of US$40,000, or 4.2%, in maintenance costs, to US$1.6 million for 2022 from US$1.6 million for 2021; |

• | an increase of US$0.3 million or 8.1% in other property related expenses. |

• | a US$0.2 million decrease in real estate taxes, to US$0.3 million for the year ended December 31, 2022 from US$0.5 million for the year ended December 31, 2021; |

• | a US$0.4 million increase in other property related expenses. |

• | US$16.1 million related to a benefit for: (i) the effect of changes in exchange rates used to convert the carrying amount of our assets (including investment property and net tax loss carryforwards) for tax purposes, from Mexican pesos to U.S. dollars, as of the end of the year, (ii) a benefit from the impact of inflation on the carrying amount of our assets (including investment property and net tax loss carryforwards) for tax purposes, as allowed by the Mexican Income Tax Law (Ley del Impuesto Sobre la Renta), and (iii) the effects of the recognition of the fair value of our investment property for accounting purposes, since the carrying amount for tax purposes remains a historical cost and is subsequently depreciated; |

• | US$4.3 million related to a benefit for the updated treatment of debt issuance cost according to tax rules applicable for 2022; |

• | US$1.2 million benefit resulting from the derecognition of forward contract deferrals during 2022; and |

• | US$3.3 million benefit related to currency translation of WTN. |

• | US$0.4 million benefit related to the decrease on our reserves on lease receivables. |

• | US$0.2 million benefit related to a larger accrual of employee benefits. |

| | | For the Three-Month Period Ended March 31, | | | For the Year Ended December 31, | |||||||

| | | 2023 | | | 2022 | | | 2022 | | | 2021 | |

| | | | | | | (millions of US$) | ||||||

Net cash generated (used) by operating activities | | | 24.1 | | | (4.7) | | | 65.2 | | | 107.9 |

Net cash (used) generated by investing activities | | | (46.7) | | | (80.6) | | | (262.2) | | | 16.0 |

Net cash (used) generated by financing activities | | | (22.8) | | | (28.0) | | | (119.8) | | | 212.5 |

Effects of exchange rates changes on cash | | | 4.5 | | | 3.0 | | | 3.1 | | | (4.2) |

Net (decrease) increase in cash, cash equivalents and restricted cash | | | (40.9) | | | (110.3) | | | (313.7) | | | 332.3 |

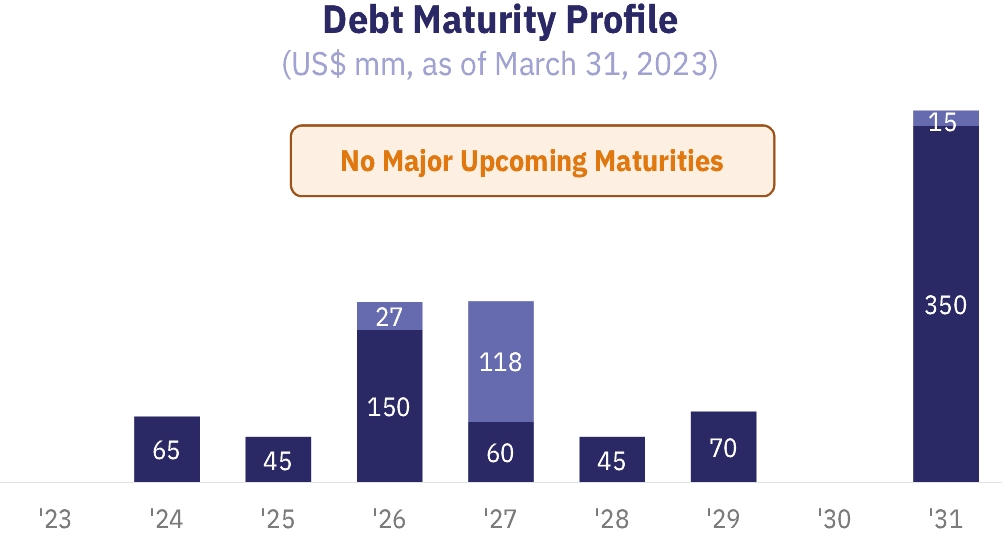

| | | Original Principal Amount | | | | | | | Principal Amount Outstanding as of March 31, | ||||||

| | | Annual Interest Rate | | | Maturity | | | 2023 | | | 2022 | ||||

| | | (millions of US$) | | | | | | | (millions of US$) | ||||||

Loan/Notes | | | | | | | | | | | |||||

2016 MetLife 10-year Loan | | | 150.0 | | | 4.55% | | | Aug. 2026 | | | 146.1 | | | 146.7 |

2017 Series A Senior Notes | | | 65.0 | | | 5.03% | | | Sept. 2024 | | | 65.0 | | | 65.0 |

2017 Series B Senior Notes | | | 60.0 | | | 5.31% | | | Sept. 2027 | | | 60.0 | | | 60.0 |

2018 Series A Senior Notes | | | 45.0 | | | 5.50% | | | May 2025 | | | 45.0 | | | 45.0 |

2018 Series B Senior Notes | | | 45.0 | | | 5.85% | | | May 2028 | | | 45.0 | | | 45.0 |

2017 MetLife 10-year Loan | | | 118.0 | | | 4.75% | | | Dec. 2027 | | | 117.4 | | | 118.0 |

2018 MetLife 8-year Loan | | | 26.6 | | | 4.75% | | | Aug. 2026 | | | 26.0 | | | 26.0 |

Series RC Senior Notes | | | 70.0 | | | 5.18% | | | June 2029 | | | 70.0 | | | 70.0 |

Series RD Senior Notes | | | 15.0 | | | 5.28% | | | June 2031 | | | 15.0 | | | 15.0 |

Sustainability-linked Senior Notes | | | 350.0 | | | 3.625% | | | May 2031 | | | 350.0 | | | 350.0 |

Sustainability-linked Revolving Credit Facility | | | 200.0 | | | SOFR plus 160 basis points(1) | | | Aug. 2025 | | | — | | | — |

| | | | | | | | | 939.4 | | | 940.6 | ||||

(-) Less: Current portion | | | | | | | | | (4.6) | | | (4.6) | |||

(-) Less: Direct issuance cost | | | | | | | | | (9.8) | | | (10.1) | |||

Total long-term debt | | | | | | | | | 925.0 | | | 925.9 | |||

(1) | Interest rate may increase if our leverage ratio exceeds 40.0%. For more information, see “—Sustainability-linked Revolving Credit Facility.” |

• | merge with or into another entity; |

• | undergo a change of control; |

• | incur additional indebtedness and liens, subject to certain exceptions; |

• | make asset sales, subject to certain exceptions; |

• | make dividend and similar payments and prepayments of certain unsecured indebtedness; and |

• | make investments in any of the following types of properties if the applicable percentage of our total asset value set forth below pertaining to such type of investment would be exceeded immediately following that investment: |

• | investments in raw or undeveloped land exceeding in aggregate 15% of our total asset value; |

• | investments in development properties exceeding in aggregate 20.0% of our total asset value; |

• | investments in joint ventures exceeding in aggregate 10.0% of our total asset value; |

• | investments in direct and indirect interests in real property (other than as stated above) exceeding in aggregate 3% of our total asset value; and |

• | investments in any of the types of property described above exceeding in aggregate 35% of our total asset value. |

• | maintain the collateral securing the notes; |

• | comply with reporting requirements in connection with our financial and operational results; |

• | maintain the following financial ratios: |

• | a minimum equity value of not less than (i) US$848.8 million, plus (ii) 70.0% of the net proceeds of all offerings of our equity interests (excluding any net proceeds applied to repurchases of any of our equity interests) at all times; |

• | a leverage ratio not exceeding 50.0% on any test date; |

• | a ratio of secured debt to total asset value not exceeding 40.0% on any test date; |

• | a ratio of unsecured debt to unencumbered asset value not exceeding 50.0% on any test date; |

• | a fixed charge coverage ratio greater than 1.5 to 1.0 on any test date; and |

• | a ratio of unencumbered property adjusted net operating income to debt service greater than 1.6 to 1.0 on any test date. |

| | | | | Payments Due by Period | |||||||||||

| | | Total | | | Less than 1 year | | | 1 to 3 years | | | 3 to 5 years | | | More than 5 years | |

| | | | | | | (millions of US$) | | | |||||||

Current portion of long-term debt | | | 4.6 | | | 4.6 | | | — | | | — | | | — |

Long-term debt | | | 925.0 | | | — | | | 4.9 | | | 449.8 | | | 470.3 |

Total | | | 929.6(1) | | | 4.6 | | | 4.9 | | | 449.8 | | | 470.3 |

(1) | Includes debt issuance costs. |

| | | For the Three-Month Period Ended March 31, | | | For the Year Ended December 31, | |||||||

| | | 2023 | | | 2022 | | | 2022 | | | 2021 | |

| | | | | (millions of US$) | | | ||||||

Profit or loss impact: | | | | | | | | | ||||

Peso – 10.0% appreciation – gain | | | 0.5 | | | 0.3 | | | 0.2 | | | (0.2) |

Peso – 10.0% depreciation – loss | | | (0.6) | | | (0.4) | | | (0.2) | | | 0.3 |

U.S. dollar – 10.0% appreciation – loss | | | (55.2) | | | (62.3) | | | (59.5) | | | (65.0) |

U.S. dollar – 10.0% appreciation – gain | | | 55.2 | | | 62.3 | | | 59.5 | | | 65.0 |

• | our business and strategy of investment strategy of investing in industrial facilities, which may subject us to risks of the sector in which we operate but uncommon to other companies that invest primarily in a broader range of real estate assets; |

• | our ability to maintain or increase our rental rates and occupancy rates; |

• | the performance and financial condition of our tenants; |

• | our expectations regarding income, expenses, sales, operations and profitability; |

• | higher interest rates, increased leasing costs, increased construction costs, distressed supply chains for construction materials, increased maintenance costs, all of which could increase our costs and limit our ability to acquire or develop additional real estate assets; |

• | our ability to obtain returns from our projects similar or comparable to those obtained in the past; |

• | our ability to successfully expand into new markets in Mexico; |

• | our ability to successfully engage in property development; |

• | our ability to lease or sell any of our properties; |

• | our ability to successfully acquire land or properties to be able to execute on our accelerated growth strategy; |

• | the competition within our industry and markets in which we operate; |

• | economic trends in the industries or the markets in which our customers operate; |

• | the continuing impact of the COVID-19 pandemic and the impact of any other pandemics, epidemics or outbreaks of infectious diseases on the Mexican economy and on our business, results of operations, financial condition, cash flows and prospects, as well as our ability to implement any necessary measures in response to such impact; |

• | loss of any significant customers; |

• | the terms of laws and government regulations that affect us, and interpretations of those laws and regulations, including changes in tax laws and regulations applicable to our subsidiaries, such as increases in real property tax rates, and changes in environmental, labor, real estate and zoning laws; |

• | deterioration of labor relations with third-party contractors, changes in labor costs and labor difficulties, including subcontracting reforms in Mexico comprising changes to labor and social laws; |