false2023FY0001969373O500019693732023-01-012023-12-310001969373dei:BusinessContactMember2023-01-012023-12-310001969373vtmx:AmericanDepositarySharesMember2023-01-012023-12-310001969373ifrs-full:OrdinarySharesMember2023-01-012023-12-3100019693732023-12-31xbrli:sharesiso4217:USD00019693732022-12-3100019693732021-12-3100019693732022-01-012022-12-3100019693732021-01-012021-12-31iso4217:USDxbrli:shares0001969373ifrs-full:IssuedCapitalMember2020-12-310001969373ifrs-full:AdditionalPaidinCapitalMember2020-12-310001969373ifrs-full:RetainedEarningsMember2020-12-310001969373ifrs-full:ReserveOfSharebasedPaymentsMember2020-12-310001969373ifrs-full:ReserveOfExchangeDifferencesOnTranslationMember2020-12-310001969373vtmx:ValuationOfDerivativeFinancialInstrumentsMember2020-12-3100019693732020-12-310001969373ifrs-full:IssuedCapitalMember2021-01-012021-12-310001969373ifrs-full:AdditionalPaidinCapitalMember2021-01-012021-12-310001969373ifrs-full:ReserveOfSharebasedPaymentsMember2021-01-012021-12-310001969373ifrs-full:RetainedEarningsMember2021-01-012021-12-310001969373ifrs-full:ReserveOfExchangeDifferencesOnTranslationMember2021-01-012021-12-310001969373vtmx:ValuationOfDerivativeFinancialInstrumentsMember2021-01-012021-12-310001969373ifrs-full:IssuedCapitalMember2021-12-310001969373ifrs-full:AdditionalPaidinCapitalMember2021-12-310001969373ifrs-full:RetainedEarningsMember2021-12-310001969373ifrs-full:ReserveOfSharebasedPaymentsMember2021-12-310001969373ifrs-full:ReserveOfExchangeDifferencesOnTranslationMember2021-12-310001969373vtmx:ValuationOfDerivativeFinancialInstrumentsMember2021-12-310001969373ifrs-full:ReserveOfSharebasedPaymentsMember2022-01-012022-12-310001969373ifrs-full:IssuedCapitalMember2022-01-012022-12-310001969373ifrs-full:AdditionalPaidinCapitalMember2022-01-012022-12-310001969373ifrs-full:RetainedEarningsMember2022-01-012022-12-310001969373ifrs-full:ReserveOfExchangeDifferencesOnTranslationMember2022-01-012022-12-310001969373ifrs-full:IssuedCapitalMember2022-12-310001969373ifrs-full:AdditionalPaidinCapitalMember2022-12-310001969373ifrs-full:RetainedEarningsMember2022-12-310001969373ifrs-full:ReserveOfSharebasedPaymentsMember2022-12-310001969373ifrs-full:ReserveOfExchangeDifferencesOnTranslationMember2022-12-310001969373vtmx:ValuationOfDerivativeFinancialInstrumentsMember2022-12-310001969373ifrs-full:IssuedCapitalMember2023-01-012023-12-310001969373ifrs-full:AdditionalPaidinCapitalMember2023-01-012023-12-310001969373ifrs-full:ReserveOfSharebasedPaymentsMember2023-01-012023-12-310001969373ifrs-full:RetainedEarningsMember2023-01-012023-12-310001969373ifrs-full:ReserveOfExchangeDifferencesOnTranslationMember2023-01-012023-12-310001969373vtmx:ValuationOfDerivativeFinancialInstrumentsMember2023-01-012023-12-310001969373ifrs-full:IssuedCapitalMember2023-12-310001969373ifrs-full:AdditionalPaidinCapitalMember2023-12-310001969373ifrs-full:RetainedEarningsMember2023-12-310001969373ifrs-full:ReserveOfSharebasedPaymentsMember2023-12-310001969373ifrs-full:ReserveOfExchangeDifferencesOnTranslationMember2023-12-310001969373vtmx:ValuationOfDerivativeFinancialInstrumentsMember2023-12-3100019693732021-04-272021-04-270001969373vtmx:PrimaryGlobalOfferingMember2021-04-272021-04-270001969373vtmx:OverAllotmentOption1Member2021-04-27xbrli:pure00019693732021-04-270001969373vtmx:OverAllotmentOption1Member2022-04-282022-04-280001969373vtmx:SeniorNotesVestaESGGlobalBondMember2021-05-130001969373vtmx:SeniorNotesVestaESGGlobalBondMember2021-05-132021-05-130001969373vtmx:SustainabilityLinkedRevolvingCreditFacilityMember2022-09-010001969373vtmx:SustainabilityLinkedRevolvingCreditFacilityMember2022-09-012022-09-010001969373vtmx:SustainabilityLinkedRevolvingCreditFacilityMember2023-12-3100019693732020-01-012020-12-31vtmx:deferralAgreement00019693732021-09-300001969373vtmx:InitialPublicOfferingOfferingMembervtmx:AmericanDepositarySharesMember2023-06-292023-06-2900019693732023-06-292023-06-290001969373vtmx:OverAllotmentOption1Member2023-06-292023-06-290001969373vtmx:AmericanDepositarySharesMember2023-06-290001969373vtmx:InitialPublicOfferingOfferingMember2023-07-052023-07-050001969373vtmx:OverAllotmentOption1Member2023-07-052023-07-050001969373vtmx:FollowOnOfferingMember2023-12-072023-12-070001969373vtmx:FollowOnOfferingMembervtmx:AmericanDepositarySharesMember2023-12-070001969373vtmx:FollowOnOfferingMember2023-12-132023-12-130001969373vtmx:QVCS.DeR.L.DeC.V.Member2023-01-012023-12-310001969373vtmx:QVCS.DeR.L.DeC.V.Member2022-01-012022-12-310001969373vtmx:QVCS.DeR.L.DeC.V.Member2021-01-012021-12-310001969373vtmx:QVCIIS.DeR.L.DeC.V.Member2023-01-012023-12-310001969373vtmx:QVCIIS.DeR.L.DeC.V.Member2022-01-012022-12-310001969373vtmx:QVCIIS.DeR.L.DeC.V.Member2021-01-012021-12-310001969373vtmx:WTNDesarrollosInmobiliariosDeMexicoS.DeR.L.DeC.V.Member2023-01-012023-12-310001969373vtmx:WTNDesarrollosInmobiliariosDeMexicoS.DeR.L.DeC.V.Member2022-01-012022-12-310001969373vtmx:WTNDesarrollosInmobiliariosDeMexicoS.DeR.L.DeC.V.Member2021-01-012021-12-310001969373vtmx:VestaBajaCaliforniaS.DeR.L.DeC.V.Member2023-01-012023-12-310001969373vtmx:VestaBajaCaliforniaS.DeR.L.DeC.V.Member2022-01-012022-12-310001969373vtmx:VestaBajaCaliforniaS.DeR.L.DeC.V.Member2021-01-012021-12-310001969373vtmx:VestaBajioS.DeR.L.DeC.V.Member2023-01-012023-12-310001969373vtmx:VestaBajioS.DeR.L.DeC.V.Member2022-01-012022-12-310001969373vtmx:VestaBajioS.DeR.L.DeC.V.Member2021-01-012021-12-310001969373vtmx:VestaQueretaroS.DeR.L.DeC.V.Member2023-01-012023-12-310001969373vtmx:VestaQueretaroS.DeR.L.DeC.V.Member2022-01-012022-12-310001969373vtmx:VestaQueretaroS.DeR.L.DeC.V.Member2021-01-012021-12-310001969373vtmx:ProyectosAeroespacialesS.DeR.L.DeC.V.Member2023-01-012023-12-310001969373vtmx:ProyectosAeroespacialesS.DeR.L.DeC.V.Member2022-01-012022-12-310001969373vtmx:ProyectosAeroespacialesS.DeR.L.DeC.V.Member2021-01-012021-12-310001969373vtmx:VestaDSPS.DeR.L.DeC.V.Member2023-01-012023-12-310001969373vtmx:VestaDSPS.DeR.L.DeC.V.Member2022-01-012022-12-310001969373vtmx:VestaDSPS.DeR.L.DeC.V.Member2021-01-012021-12-310001969373vtmx:VestaManagementS.DeR.L.DeC.V.Member2023-01-012023-12-310001969373vtmx:VestaManagementS.DeR.L.DeC.V.Member2022-01-012022-12-310001969373vtmx:VestaManagementS.DeR.L.DeC.V.Member2021-01-012021-12-310001969373vtmx:ServicioDeAdministracionYMantenimientoVestaS.DeR.L.DeC.V.Member2023-01-012023-12-310001969373vtmx:ServicioDeAdministracionYMantenimientoVestaS.DeR.L.DeC.V.Member2022-01-012022-12-310001969373vtmx:ServicioDeAdministracionYMantenimientoVestaS.DeR.L.DeC.V.Member2021-01-012021-12-310001969373vtmx:EnervestaS.DeR.L.DeC.V.Member2023-01-012023-12-310001969373vtmx:EnervestaS.DeR.L.DeC.V.Member2022-01-012022-12-310001969373vtmx:EnervestaS.DeR.L.DeC.V.Member2021-01-012021-12-31vtmx:investmentProperty0001969373ifrs-full:LandMember2022-07-012022-09-300001969373ifrs-full:LandMember2022-09-300001969373ifrs-full:GrossCarryingAmountMember2023-01-012023-12-310001969373ifrs-full:GrossCarryingAmountMember2022-01-012022-12-310001969373ifrs-full:GrossCarryingAmountMember2021-01-012021-12-310001969373vtmx:A030DaysMember2023-12-310001969373vtmx:A030DaysMember2022-12-310001969373vtmx:A030DaysMember2021-12-310001969373vtmx:A3060DaysMember2023-12-310001969373vtmx:A3060DaysMember2022-12-310001969373vtmx:A3060DaysMember2021-12-310001969373vtmx:A6090DaysMember2023-12-310001969373vtmx:A6090DaysMember2022-12-310001969373vtmx:A6090DaysMember2021-12-310001969373vtmx:Over90DaysMember2023-12-310001969373vtmx:Over90DaysMember2022-12-310001969373vtmx:Over90DaysMember2021-12-310001969373vtmx:OneCustomerMemberifrs-full:LeaseReceivablesMemberifrs-full:MajorCustomersMember2023-01-012023-12-310001969373vtmx:OneCustomerMemberifrs-full:LeaseReceivablesMemberifrs-full:MajorCustomersMember2023-12-310001969373vtmx:OneCustomerMemberifrs-full:LeaseReceivablesMemberifrs-full:MajorCustomersMember2022-01-012022-12-310001969373vtmx:OneCustomerMemberifrs-full:LeaseReceivablesMemberifrs-full:MajorCustomersMember2022-12-310001969373vtmx:OneCustomerMemberifrs-full:LeaseReceivablesMemberifrs-full:MajorCustomersMember2021-01-012021-12-310001969373vtmx:OneCustomerMemberifrs-full:LeaseReceivablesMemberifrs-full:MajorCustomersMember2021-12-310001969373vtmx:OneCustomerMemberifrs-full:MajorCustomersMembervtmx:RentalIncomeMember2023-01-012023-12-310001969373vtmx:OneCustomerMemberifrs-full:MajorCustomersMembervtmx:RentalIncomeMember2022-01-012022-12-310001969373vtmx:OneCustomerMemberifrs-full:MajorCustomersMembervtmx:RentalIncomeMember2021-01-012021-12-310001969373ifrs-full:BottomOfRangeMember2023-12-310001969373ifrs-full:TopOfRangeMember2023-12-310001969373ifrs-full:NotLaterThanOneYearMember2023-12-310001969373ifrs-full:NotLaterThanOneYearMember2022-12-310001969373ifrs-full:NotLaterThanOneYearMember2021-12-310001969373ifrs-full:LaterThanOneYearAndNotLaterThanThreeYearsMember2023-12-310001969373ifrs-full:LaterThanOneYearAndNotLaterThanThreeYearsMember2022-12-310001969373ifrs-full:LaterThanOneYearAndNotLaterThanThreeYearsMember2021-12-310001969373ifrs-full:LaterThanThreeYearsAndNotLaterThanFiveYearsMember2023-12-310001969373ifrs-full:LaterThanThreeYearsAndNotLaterThanFiveYearsMember2022-12-310001969373ifrs-full:LaterThanThreeYearsAndNotLaterThanFiveYearsMember2021-12-310001969373ifrs-full:LaterThanFiveYearsMember2023-12-310001969373ifrs-full:LaterThanFiveYearsMember2022-12-310001969373ifrs-full:LaterThanFiveYearsMember2021-12-3100019693732022-04-012022-06-3000019693732022-06-300001969373vtmx:LandReserveInQueretaroMember2022-12-310001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:LandAndBuildingsMemberifrs-full:DiscountRateMeasurementInputMemberifrs-full:DiscountedCashFlowMemberifrs-full:BottomOfRangeMember2023-12-310001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:TopOfRangeMemberifrs-full:LandAndBuildingsMemberifrs-full:DiscountRateMeasurementInputMemberifrs-full:DiscountedCashFlowMember2023-12-310001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:LandAndBuildingsMemberifrs-full:DiscountRateMeasurementInputMemberifrs-full:DiscountedCashFlowMemberifrs-full:BottomOfRangeMember2022-12-310001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:TopOfRangeMemberifrs-full:LandAndBuildingsMemberifrs-full:DiscountRateMeasurementInputMemberifrs-full:DiscountedCashFlowMember2022-12-310001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:LandAndBuildingsMemberifrs-full:DiscountRateMeasurementInputMemberifrs-full:DiscountedCashFlowMemberifrs-full:BottomOfRangeMember2021-12-310001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:TopOfRangeMemberifrs-full:LandAndBuildingsMemberifrs-full:DiscountRateMeasurementInputMemberifrs-full:DiscountedCashFlowMember2021-12-310001969373ifrs-full:Level3OfFairValueHierarchyMembervtmx:ExitCapRateMeasurementInputMemberifrs-full:LandAndBuildingsMemberifrs-full:DiscountedCashFlowMemberifrs-full:BottomOfRangeMember2023-12-310001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:TopOfRangeMembervtmx:ExitCapRateMeasurementInputMemberifrs-full:LandAndBuildingsMemberifrs-full:DiscountedCashFlowMember2023-12-310001969373ifrs-full:Level3OfFairValueHierarchyMembervtmx:ExitCapRateMeasurementInputMemberifrs-full:LandAndBuildingsMemberifrs-full:DiscountedCashFlowMemberifrs-full:BottomOfRangeMember2022-12-310001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:TopOfRangeMembervtmx:ExitCapRateMeasurementInputMemberifrs-full:LandAndBuildingsMemberifrs-full:DiscountedCashFlowMember2022-12-310001969373ifrs-full:Level3OfFairValueHierarchyMembervtmx:ExitCapRateMeasurementInputMemberifrs-full:LandAndBuildingsMemberifrs-full:DiscountedCashFlowMemberifrs-full:BottomOfRangeMember2021-12-310001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:TopOfRangeMembervtmx:ExitCapRateMeasurementInputMemberifrs-full:LandAndBuildingsMemberifrs-full:DiscountedCashFlowMember2021-12-310001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:LandAndBuildingsMembercountry:MXvtmx:InflationRatesMeasurementInputMemberifrs-full:DiscountedCashFlowMemberifrs-full:BottomOfRangeMember2023-12-310001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:TopOfRangeMemberifrs-full:LandAndBuildingsMembercountry:MXvtmx:InflationRatesMeasurementInputMemberifrs-full:DiscountedCashFlowMember2023-12-310001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:LandAndBuildingsMembercountry:MXvtmx:InflationRatesMeasurementInputMemberifrs-full:DiscountedCashFlowMemberifrs-full:BottomOfRangeMember2022-12-310001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:TopOfRangeMemberifrs-full:LandAndBuildingsMembercountry:MXvtmx:InflationRatesMeasurementInputMemberifrs-full:DiscountedCashFlowMember2022-12-310001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:LandAndBuildingsMembercountry:MXvtmx:InflationRatesMeasurementInputMemberifrs-full:DiscountedCashFlowMemberifrs-full:BottomOfRangeMember2021-12-310001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:TopOfRangeMemberifrs-full:LandAndBuildingsMembercountry:MXvtmx:InflationRatesMeasurementInputMemberifrs-full:DiscountedCashFlowMember2021-12-310001969373country:USifrs-full:Level3OfFairValueHierarchyMemberifrs-full:LandAndBuildingsMembervtmx:InflationRatesMeasurementInputMemberifrs-full:DiscountedCashFlowMemberifrs-full:BottomOfRangeMember2023-12-310001969373country:USifrs-full:Level3OfFairValueHierarchyMemberifrs-full:TopOfRangeMemberifrs-full:LandAndBuildingsMembervtmx:InflationRatesMeasurementInputMemberifrs-full:DiscountedCashFlowMember2023-12-310001969373country:USifrs-full:Level3OfFairValueHierarchyMemberifrs-full:LandAndBuildingsMembervtmx:InflationRatesMeasurementInputMemberifrs-full:DiscountedCashFlowMemberifrs-full:BottomOfRangeMember2022-12-310001969373country:USifrs-full:Level3OfFairValueHierarchyMemberifrs-full:TopOfRangeMemberifrs-full:LandAndBuildingsMembervtmx:InflationRatesMeasurementInputMemberifrs-full:DiscountedCashFlowMember2022-12-310001969373country:USifrs-full:Level3OfFairValueHierarchyMemberifrs-full:LandAndBuildingsMembervtmx:InflationRatesMeasurementInputMemberifrs-full:DiscountedCashFlowMemberifrs-full:BottomOfRangeMember2021-12-310001969373country:USifrs-full:Level3OfFairValueHierarchyMemberifrs-full:TopOfRangeMemberifrs-full:LandAndBuildingsMembervtmx:InflationRatesMeasurementInputMemberifrs-full:DiscountedCashFlowMember2021-12-310001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:MarketComparablePricesMembervtmx:LandReservesMembervtmx:PricePerAcreMeasurementInputMember2023-12-31iso4217:USDutr:acre0001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:MarketComparablePricesMembervtmx:LandReservesMembervtmx:PricePerAcreMeasurementInputMember2022-12-310001969373ifrs-full:Level3OfFairValueHierarchyMemberifrs-full:MarketComparablePricesMembervtmx:LandReservesMembervtmx:PricePerAcreMeasurementInputMember2021-12-310001969373vtmx:ExitCapRateMeasurementInputMember2023-01-012023-12-310001969373ifrs-full:DiscountRateMeasurementInputMember2023-01-012023-12-310001969373vtmx:ExitCapRateAndDiscountRateMember2023-01-012023-12-310001969373vtmx:ExitCapRateMeasurementInputMember2022-01-012022-12-310001969373ifrs-full:DiscountRateMeasurementInputMember2022-01-012022-12-310001969373vtmx:ExitCapRateAndDiscountRateMember2022-01-012022-12-310001969373vtmx:ExitCapRateMeasurementInputMember2021-01-012021-12-310001969373ifrs-full:DiscountRateMeasurementInputMember2021-01-012021-12-310001969373vtmx:ExitCapRateAndDiscountRateMember2021-01-012021-12-310001969373ifrs-full:LandAndBuildingsMember2023-12-310001969373ifrs-full:LandAndBuildingsMember2022-12-310001969373ifrs-full:LandAndBuildingsMember2021-12-310001969373vtmx:LandImprovementsMember2023-12-310001969373vtmx:LandImprovementsMember2022-12-310001969373vtmx:LandImprovementsMember2021-12-310001969373vtmx:LandReservesMember2023-12-310001969373vtmx:LandReservesMember2022-12-310001969373vtmx:LandReservesMember2021-12-310001969373vtmx:LandReservesAndNewBuildingsMember2023-01-012023-12-310001969373vtmx:LandReservesAndNewBuildingsMember2022-01-012022-12-310001969373vtmx:LandReservesAndNewBuildingsMember2021-01-012021-12-310001969373vtmx:AguascalientesMembervtmx:LandReservesMember2023-01-012023-12-31utr:sqft0001969373vtmx:TijuanaMemberifrs-full:BuildingsMember2023-01-012023-12-310001969373vtmx:AguascalientesAndTijuanaMembervtmx:LandReservesAndNewBuildingsMember2023-12-310001969373vtmx:AguascalientesAndTijuanaMembervtmx:LandReservesAndNewBuildingsMember2023-01-012023-12-310001969373vtmx:QueretaroMembervtmx:LandReservesMember2022-01-012022-12-31vtmx:landReserve0001969373vtmx:Cd.JuarezMembervtmx:LandReservesMember2022-01-012022-12-310001969373vtmx:LandReservesMember2022-01-012022-12-310001969373vtmx:QueretaroAndCd.JuarezMembervtmx:LandReservesMember2022-01-012022-12-31vtmx:sale0001969373vtmx:QueretaroAndCd.JuarezMembervtmx:LandReservesMember2022-12-310001969373vtmx:QueretaroMembervtmx:LandReservesMember2021-01-012021-12-310001969373vtmx:QueretaroMembervtmx:LandReservesMember2021-12-310001969373vtmx:QueretaroAndCiudadJuarezMembervtmx:IndustrialPropertiesMember2021-01-012021-12-31vtmx:industrialProperty0001969373vtmx:QueretaroAndCiudadJuarezMembervtmx:IndustrialPropertiesMember2021-12-310001969373vtmx:QueretaroAerospaceParkMember2023-01-012023-12-310001969373vtmx:QueretaroAerospaceParkAirportConcessionsMember2023-01-012023-12-310001969373vtmx:NissanTheDoukiSeisanParkMember2023-01-012023-12-310001969373vtmx:CollateralPledged1Member2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:OfficeSpaceMember2022-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:OfficeSpaceMember2023-01-012023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:OfficeSpaceMember2023-12-310001969373vtmx:VehiclesAndOfficeFurnitureMemberifrs-full:GrossCarryingAmountMember2022-12-310001969373vtmx:VehiclesAndOfficeFurnitureMemberifrs-full:GrossCarryingAmountMember2023-01-012023-12-310001969373vtmx:VehiclesAndOfficeFurnitureMemberifrs-full:GrossCarryingAmountMember2023-12-310001969373ifrs-full:GrossCarryingAmountMember2022-12-310001969373ifrs-full:GrossCarryingAmountMember2023-12-310001969373vtmx:OfficeSpaceMemberifrs-full:AccumulatedDepreciationAndAmortisationMember2022-12-310001969373vtmx:OfficeSpaceMemberifrs-full:AccumulatedDepreciationAndAmortisationMember2023-01-012023-12-300001969373vtmx:OfficeSpaceMemberifrs-full:AccumulatedDepreciationAndAmortisationMember2023-12-310001969373vtmx:VehiclesAndOfficeFurnitureMemberifrs-full:AccumulatedDepreciationAndAmortisationMember2022-12-310001969373vtmx:VehiclesAndOfficeFurnitureMemberifrs-full:AccumulatedDepreciationAndAmortisationMember2023-01-012023-12-300001969373vtmx:VehiclesAndOfficeFurnitureMemberifrs-full:AccumulatedDepreciationAndAmortisationMember2023-12-310001969373ifrs-full:AccumulatedDepreciationAndAmortisationMember2022-12-310001969373ifrs-full:AccumulatedDepreciationAndAmortisationMember2023-01-012023-12-300001969373ifrs-full:AccumulatedDepreciationAndAmortisationMember2023-12-310001969373vtmx:AdjustmentsNettingMember2023-01-012023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:OfficeSpaceMember2021-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:OfficeSpaceMember2022-01-012022-12-310001969373vtmx:VehiclesAndOfficeFurnitureMemberifrs-full:GrossCarryingAmountMember2021-12-310001969373vtmx:VehiclesAndOfficeFurnitureMemberifrs-full:GrossCarryingAmountMember2022-01-012022-12-310001969373ifrs-full:GrossCarryingAmountMember2021-12-310001969373vtmx:OfficeSpaceMemberifrs-full:AccumulatedDepreciationAndAmortisationMember2021-12-310001969373vtmx:OfficeSpaceMemberifrs-full:AccumulatedDepreciationAndAmortisationMember2022-01-012022-12-300001969373vtmx:VehiclesAndOfficeFurnitureMemberifrs-full:AccumulatedDepreciationAndAmortisationMember2021-12-310001969373vtmx:VehiclesAndOfficeFurnitureMemberifrs-full:AccumulatedDepreciationAndAmortisationMember2022-01-012022-12-300001969373ifrs-full:AccumulatedDepreciationAndAmortisationMember2021-12-310001969373ifrs-full:AccumulatedDepreciationAndAmortisationMember2022-01-012022-12-300001969373ifrs-full:GrossCarryingAmountMembervtmx:OfficeSpaceMember2020-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:OfficeSpaceMember2021-01-012021-12-310001969373vtmx:VehiclesAndOfficeFurnitureMemberifrs-full:GrossCarryingAmountMember2020-12-310001969373vtmx:VehiclesAndOfficeFurnitureMemberifrs-full:GrossCarryingAmountMember2021-01-012021-12-310001969373ifrs-full:GrossCarryingAmountMember2020-12-310001969373vtmx:OfficeSpaceMemberifrs-full:AccumulatedDepreciationAndAmortisationMember2020-12-310001969373vtmx:OfficeSpaceMemberifrs-full:AccumulatedDepreciationAndAmortisationMember2021-01-012021-12-300001969373vtmx:VehiclesAndOfficeFurnitureMemberifrs-full:AccumulatedDepreciationAndAmortisationMember2020-12-310001969373vtmx:VehiclesAndOfficeFurnitureMemberifrs-full:AccumulatedDepreciationAndAmortisationMember2021-01-012021-12-300001969373ifrs-full:AccumulatedDepreciationAndAmortisationMember2020-12-310001969373ifrs-full:AccumulatedDepreciationAndAmortisationMember2021-01-012021-12-300001969373ifrs-full:LaterThanOneYearAndNotLaterThanFiveYearsMember2023-12-310001969373ifrs-full:LaterThanOneYearAndNotLaterThanFiveYearsMember2022-12-310001969373ifrs-full:LaterThanOneYearAndNotLaterThanFiveYearsMember2021-12-310001969373vtmx:SustainabilityLinkedRevolvingCreditFacilityMembervtmx:TermSecuredOvernightFinancingRateMember2022-09-010001969373vtmx:UnsecuredCreditAgreementMember2019-08-022019-08-020001969373vtmx:UnsecuredCreditAgreementMember2019-08-020001969373vtmx:RevolvingCreditLineMember2019-08-020001969373vtmx:LondonInterBankOfferedRateMembervtmx:RevolvingCreditLineMember2019-08-020001969373vtmx:RevolvingCreditLineMember2020-03-230001969373vtmx:RevolvingCreditLineMember2020-04-070001969373vtmx:LondonInterBankOfferedRateMembervtmx:RevolvingCreditLineMember2020-03-230001969373vtmx:LondonInterBankOfferedRateMembervtmx:RevolvingCreditLineMember2020-04-070001969373vtmx:SeniorNoteSeriesRCMember2019-06-252019-06-250001969373vtmx:SeniorNoteSeriesRDMember2019-06-252019-06-250001969373vtmx:SeniorNoteSeriesRCMember2019-06-250001969373vtmx:SeniorNoteSeriesRDMember2019-06-250001969373vtmx:SeriesASeniorNote5.50DueMay2025Member2018-05-310001969373vtmx:SeriesBSeniorNote5.85DueMay2028Member2018-05-310001969373vtmx:MetLife10Year4.75LoanDueDecember2027Member2017-11-010001969373vtmx:SeriesASeniorNote5.03DueSeptember2024Member2017-09-220001969373vtmx:SeriesBSeniorNote5.31DueSeptember2027Member2017-09-220001969373vtmx:MetLife10Year4.55LoanDueAugust2026Member2016-07-272016-07-270001969373vtmx:MetLife10Year4.55LoanDueAugust2026Member2016-07-270001969373vtmx:MetLife10Year4.55LoanDueAugust2026Member2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:MetLife10Year4.55LoanDueAugust2026Member2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:MetLife10Year4.55LoanDueAugust2026Member2022-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:MetLife10Year4.55LoanDueAugust2026Member2021-12-310001969373vtmx:SeriesASeniorNote5.03DueSeptember2024Member2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeriesASeniorNote5.03DueSeptember2024Member2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeriesASeniorNote5.03DueSeptember2024Member2022-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeriesASeniorNote5.03DueSeptember2024Member2021-12-310001969373vtmx:SeriesBSeniorNote5.31DueSeptember2027Member2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeriesBSeniorNote5.31DueSeptember2027Member2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeriesBSeniorNote5.31DueSeptember2027Member2022-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeriesBSeniorNote5.31DueSeptember2027Member2021-12-310001969373vtmx:SeriesASeniorNote5.50DueMay2025Member2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeriesASeniorNote5.50DueMay2025Member2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeriesASeniorNote5.50DueMay2025Member2022-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeriesASeniorNote5.50DueMay2025Member2021-12-310001969373vtmx:SeriesBSeniorNote5.85DueMay2028Member2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeriesBSeniorNote5.85DueMay2028Member2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeriesBSeniorNote5.85DueMay2028Member2022-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeriesBSeniorNote5.85DueMay2028Member2021-12-310001969373vtmx:MetLife10Year4.75LoanDueDecember2027Member2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:MetLife10Year4.75LoanDueDecember2027Member2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:MetLife10Year4.75LoanDueDecember2027Member2022-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:MetLife10Year4.75LoanDueDecember2027Member2021-12-310001969373vtmx:MetLife8Year4.75LoanDueAugust2026Member2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:MetLife8Year4.75LoanDueAugust2026Member2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:MetLife8Year4.75LoanDueAugust2026Member2022-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:MetLife8Year4.75LoanDueAugust2026Member2021-12-310001969373vtmx:SeniorNoteSeriesRCMember2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeniorNoteSeriesRCMember2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeniorNoteSeriesRCMember2022-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeniorNoteSeriesRCMember2021-12-310001969373vtmx:SeniorNoteSeriesRDMember2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeniorNoteSeriesRDMember2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeniorNoteSeriesRDMember2022-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeniorNoteSeriesRDMember2021-12-310001969373vtmx:SeniorNotesVestaESGGlobalBondMember2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeniorNotesVestaESGGlobalBondMember2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeniorNotesVestaESGGlobalBondMember2022-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:SeniorNotesVestaESGGlobalBondMember2021-12-310001969373vtmx:DeferredFinancingCostsNettingMember2023-12-310001969373vtmx:DeferredFinancingCostsNettingMember2022-12-310001969373vtmx:DeferredFinancingCostsNettingMember2021-12-310001969373vtmx:MetLife10Year4.55LoanDueAugust2026Member2016-07-222016-07-220001969373vtmx:MetLife8Year4.75LoanDueAugust2026Member2021-03-3100019693732016-07-22vtmx:loan0001969373vtmx:MetLife10Year4.75LoanDueDecember2027Member2017-11-012017-11-010001969373vtmx:MetLife10Year4.75LoanDueDecember2027Member2023-11-280001969373vtmx:MetLife10Year4.75LoanDueDecember2027Member2023-11-282023-11-28vtmx:subsidiary0001969373ifrs-full:GrossCarryingAmountMemberifrs-full:LaterThanOneYearAndNotLaterThanTwoYearsMember2023-12-310001969373ifrs-full:GrossCarryingAmountMemberifrs-full:LaterThanTwoYearsAndNotLaterThanThreeYearsMember2023-12-310001969373ifrs-full:GrossCarryingAmountMemberifrs-full:LaterThanThreeYearsAndNotLaterThanFourYearsMember2023-12-310001969373ifrs-full:GrossCarryingAmountMemberifrs-full:LaterThanFourYearsAndNotLaterThanFiveYearsMember2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:LaterThanFiveYearsAndNotLaterThanSixYearsMember2023-12-310001969373ifrs-full:GrossCarryingAmountMembervtmx:LaterThanSixYearsMember2023-12-310001969373srt:MinimumMember2023-12-310001969373srt:MaximumMember2023-12-310001969373srt:MinimumMember2022-12-310001969373srt:MaximumMember2022-12-310001969373srt:MinimumMember2021-12-310001969373srt:MaximumMember2021-12-310001969373vtmx:SeniorityPremiumMember2023-12-310001969373vtmx:SeniorityPremiumMember2022-12-310001969373vtmx:SeniorityPremiumMember2021-12-310001969373vtmx:RetirementPlanMember2023-12-310001969373vtmx:RetirementPlanMember2022-12-310001969373vtmx:RetirementPlanMember2021-12-310001969373vtmx:SeniorityPremiumMemberifrs-full:NotLaterThanOneYearMember2023-01-012023-12-310001969373vtmx:RetirementPlanMemberifrs-full:NotLaterThanOneYearMember2023-01-012023-12-310001969373ifrs-full:LaterThanOneYearAndNotLaterThanTwoYearsMembervtmx:SeniorityPremiumMember2023-01-012023-12-310001969373ifrs-full:LaterThanOneYearAndNotLaterThanTwoYearsMembervtmx:RetirementPlanMember2023-01-012023-12-310001969373vtmx:SeniorityPremiumMemberifrs-full:LaterThanTwoYearsAndNotLaterThanThreeYearsMember2023-01-012023-12-310001969373ifrs-full:LaterThanTwoYearsAndNotLaterThanThreeYearsMembervtmx:RetirementPlanMember2023-01-012023-12-310001969373vtmx:SeniorityPremiumMemberifrs-full:LaterThanThreeYearsAndNotLaterThanFourYearsMember2023-01-012023-12-310001969373ifrs-full:LaterThanThreeYearsAndNotLaterThanFourYearsMembervtmx:RetirementPlanMember2023-01-012023-12-310001969373vtmx:SeniorityPremiumMemberifrs-full:LaterThanFourYearsAndNotLaterThanFiveYearsMember2023-01-012023-12-310001969373ifrs-full:LaterThanFourYearsAndNotLaterThanFiveYearsMembervtmx:RetirementPlanMember2023-01-012023-12-310001969373vtmx:SeniorityPremiumMemberifrs-full:LaterThanFiveYearsMember2023-01-012023-12-310001969373ifrs-full:LaterThanFiveYearsMembervtmx:RetirementPlanMember2023-01-012023-12-310001969373vtmx:FixedCapitalSeriesAStockMember2023-12-310001969373vtmx:FixedCapitalSeriesAStockMember2022-12-310001969373vtmx:FixedCapitalSeriesAStockMember2021-12-310001969373vtmx:VariableCapitalSeriesBStockMember2023-12-310001969373vtmx:VariableCapitalSeriesBStockMember2022-12-310001969373vtmx:VariableCapitalSeriesBStockMember2021-12-310001969373ifrs-full:TreasurySharesMember2023-12-310001969373ifrs-full:TreasurySharesMember2022-12-310001969373ifrs-full:TreasurySharesMember2021-12-3100019693732023-03-3000019693732023-03-302023-03-3000019693732023-04-172023-04-1700019693732023-07-172023-07-1700019693732023-10-162023-10-1600019693732022-03-2400019693732022-03-242022-03-2400019693732022-04-152022-04-1500019693732022-07-152022-07-1500019693732022-10-152022-10-1500019693732023-01-152023-01-1500019693732021-03-2300019693732021-03-232021-03-2300019693732021-04-152021-04-1500019693732021-07-152021-07-1500019693732021-10-152021-10-1500019693732022-01-152022-01-1500019693732013-12-3100019693732014-12-3100019693732016-12-3100019693732017-12-3100019693732018-12-3100019693732019-12-310001969373ifrs-full:InvestmentPropertyMember2023-12-310001969373ifrs-full:InvestmentPropertyMember2022-12-310001969373ifrs-full:InvestmentPropertyMember2021-12-310001969373ifrs-full:UnusedTaxLossesMember2023-12-310001969373ifrs-full:UnusedTaxLossesMember2022-12-310001969373ifrs-full:UnusedTaxLossesMember2021-12-310001969373ifrs-full:OtherTemporaryDifferencesMember2023-12-310001969373ifrs-full:OtherTemporaryDifferencesMember2022-12-310001969373ifrs-full:OtherTemporaryDifferencesMember2021-12-310001969373ifrs-full:CurrencyRiskMembercurrency:MXN2023-12-310001969373ifrs-full:CurrencyRiskMembercurrency:MXN2022-12-310001969373ifrs-full:CurrencyRiskMembercurrency:MXN2021-12-310001969373ifrs-full:CurrencyRiskMembercurrency:MXN2023-01-012023-12-310001969373ifrs-full:CurrencyRiskMembercurrency:MXN2022-01-012022-12-310001969373ifrs-full:CurrencyRiskMembercurrency:MXN2021-01-012021-12-310001969373ifrs-full:CurrencyRiskMembercurrency:USD2023-12-310001969373ifrs-full:CurrencyRiskMembercurrency:USD2022-12-310001969373ifrs-full:CurrencyRiskMembercurrency:USD2021-12-310001969373currency:MXN2023-01-012023-12-310001969373ifrs-full:CurrencyRiskMembercurrency:USD2023-01-012023-12-310001969373ifrs-full:CurrencyRiskMembercurrency:USD2022-01-012022-12-310001969373ifrs-full:CurrencyRiskMembercurrency:USD2021-01-012021-12-310001969373ifrs-full:LaterThanOneMonthAndNotLaterThanThreeMonthsMember2023-12-310001969373ifrs-full:LaterThanThreeMonthsAndNotLaterThanOneYearMember2023-12-310001969373vtmx:LaterThanOneYearAndNotLaterThanFourYearsMember2023-12-310001969373ifrs-full:LaterThanOneMonthAndNotLaterThanThreeMonthsMember2022-12-310001969373ifrs-full:LaterThanThreeMonthsAndNotLaterThanOneYearMember2022-12-310001969373vtmx:LaterThanOneYearAndNotLaterThanFourYearsMember2022-12-310001969373ifrs-full:LaterThanOneMonthAndNotLaterThanThreeMonthsMember2021-12-310001969373ifrs-full:LaterThanThreeMonthsAndNotLaterThanOneYearMember2021-12-310001969373vtmx:LaterThanOneYearAndNotLaterThanFourYearsMember2021-12-310001969373vtmx:BorrowingsMemberifrs-full:FinancialLiabilitiesAtAmortisedCostCategoryMember2023-12-310001969373vtmx:BorrowingsMemberifrs-full:FinancialLiabilitiesAtAmortisedCostCategoryMember2022-12-310001969373vtmx:BorrowingsMemberifrs-full:FinancialLiabilitiesAtAmortisedCostCategoryMember2021-12-31vtmx:executive0001969373vtmx:WorstPerformerMembervtmx:Level3LTIPlanMember2020-03-132020-03-130001969373vtmx:BestPerformerMembervtmx:Level3LTIPlanMember2020-03-132020-03-130001969373vtmx:Level3LTIPlanMember2020-03-132020-03-1300019693732020-03-132020-03-130001969373vtmx:Vision2020LTIPlanMember2015-01-310001969373vtmx:Level3LTIPlanMember2020-03-310001969373vtmx:GrantYearYearOneMember2023-12-310001969373vtmx:GrantYearYearOneMember2023-01-012023-12-310001969373vtmx:GrantYearYearOneMemberifrs-full:BottomOfRangeMember2023-01-012023-12-310001969373vtmx:TargetMembervtmx:GrantYearYearOneMember2023-01-012023-12-310001969373ifrs-full:TopOfRangeMembervtmx:GrantYearYearOneMember2023-01-012023-12-310001969373vtmx:GrantYearYearTwoMember2023-12-310001969373vtmx:GrantYearYearTwoMember2023-01-012023-12-310001969373vtmx:GrantYearYearTwoMemberifrs-full:BottomOfRangeMember2023-01-012023-12-310001969373vtmx:TargetMembervtmx:GrantYearYearTwoMember2023-01-012023-12-310001969373vtmx:GrantYearYearTwoMemberifrs-full:TopOfRangeMember2023-01-012023-12-310001969373vtmx:GrantYearYearThreeMember2023-12-310001969373vtmx:GrantYearYearThreeMember2023-01-012023-12-310001969373vtmx:GrantYearYearThreeMemberifrs-full:BottomOfRangeMember2023-01-012023-12-310001969373vtmx:TargetMembervtmx:GrantYearYearThreeMember2023-01-012023-12-310001969373vtmx:GrantYearYearThreeMemberifrs-full:TopOfRangeMember2023-01-012023-12-310001969373vtmx:GrantYearYearFourMember2023-12-310001969373vtmx:GrantYearYearFourMember2023-01-012023-12-310001969373vtmx:GrantYearYearFourMemberifrs-full:BottomOfRangeMember2023-01-012023-12-310001969373vtmx:TargetMembervtmx:GrantYearYearFourMember2023-01-012023-12-310001969373vtmx:GrantYearYearFourMemberifrs-full:TopOfRangeMember2023-01-012023-12-310001969373vtmx:GrantYearYearFiveMember2023-12-310001969373vtmx:GrantYearYearFiveMember2023-01-012023-12-310001969373vtmx:GrantYearYearFiveMemberifrs-full:BottomOfRangeMember2023-01-012023-12-310001969373vtmx:GrantYearYearFiveMembervtmx:TargetMember2023-01-012023-12-310001969373vtmx:GrantYearYearFiveMemberifrs-full:TopOfRangeMember2023-01-012023-12-310001969373vtmx:GrantYearYearSixMember2023-12-310001969373vtmx:GrantYearYearSixMember2023-01-012023-12-310001969373vtmx:GrantYearYearSixMemberifrs-full:BottomOfRangeMember2023-01-012023-12-310001969373vtmx:TargetMembervtmx:GrantYearYearSixMember2023-01-012023-12-310001969373ifrs-full:TopOfRangeMembervtmx:GrantYearYearSixMember2023-01-012023-12-310001969373vtmx:GrantYearYearSevenMember2023-12-310001969373vtmx:GrantYearYearSevenMember2023-01-012023-12-310001969373vtmx:GrantYearYearSevenMemberifrs-full:BottomOfRangeMember2023-01-012023-12-310001969373vtmx:TargetMembervtmx:GrantYearYearSevenMember2023-01-012023-12-310001969373ifrs-full:TopOfRangeMembervtmx:GrantYearYearSevenMember2023-01-012023-12-310001969373vtmx:GrantYearYearEightMember2023-12-310001969373vtmx:GrantYearYearEightMember2023-01-012023-12-310001969373vtmx:GrantYearYearEightMemberifrs-full:BottomOfRangeMember2023-01-012023-12-310001969373vtmx:GrantYearYearEightMembervtmx:TargetMember2023-01-012023-12-310001969373vtmx:GrantYearYearEightMemberifrs-full:TopOfRangeMember2023-01-012023-12-310001969373vtmx:GrantYearYearNineMember2023-12-310001969373vtmx:GrantYearYearNineMember2023-01-012023-12-310001969373vtmx:GrantYearYearNineMemberifrs-full:BottomOfRangeMember2023-01-012023-12-310001969373vtmx:TargetMembervtmx:GrantYearYearNineMember2023-01-012023-12-310001969373vtmx:GrantYearYearNineMemberifrs-full:TopOfRangeMember2023-01-012023-12-310001969373vtmx:Level3LTIPlanMember2023-01-012023-12-310001969373vtmx:Level3LTIPlanMember2022-01-012022-12-310001969373vtmx:Level3LTIPlanMember2021-01-012021-12-310001969373ifrs-full:MajorOrdinaryShareTransactionsMember2024-01-152024-01-150001969373ifrs-full:OtherDisposalsOfAssetsMember2024-01-242024-01-240001969373vtmx:OperatingParkDSPAguascalientesMember2023-01-012023-12-31vtmx:building0001969373vtmx:OperatingParkDSPAguascalientesMember2023-12-310001969373vtmx:OperatingParkVestaParkAguascalientesAguascalientesMember2023-01-012023-12-310001969373vtmx:OperatingParkVestaParkAguascalientesAguascalientesMember2023-12-310001969373vtmx:OperatingParkLosBravosVestaParkCdJuarezMember2023-01-012023-12-310001969373vtmx:OperatingParkLosBravosVestaParkCdJuarezMember2023-12-310001969373vtmx:OperatingParkVestaParkJuarezSurICdJuarezMember2023-01-012023-12-310001969373vtmx:OperatingParkVestaParkJuarezSurICdJuarezMember2023-12-310001969373vtmx:OperatingParkVestaParkGuadalajaraGuadalajaraMember2023-01-012023-12-310001969373vtmx:OperatingParkVestaParkGuadalajaraGuadalajaraMember2023-12-310001969373vtmx:OperatingParkVestaParkGuadalupeMonterreyMember2023-01-012023-12-310001969373vtmx:OperatingParkVestaParkGuadalupeMonterreyMember2023-12-310001969373vtmx:OperatingParkVestaPueblaIPueblaMember2023-01-012023-12-310001969373vtmx:OperatingParkVestaPueblaIPueblaMember2023-12-310001969373vtmx:OperatingParkBernardoQuintanaQueretaroMember2023-01-012023-12-310001969373vtmx:OperatingParkBernardoQuintanaQueretaroMember2023-12-310001969373vtmx:OperatingParkPIQQueretaroMember2023-01-012023-12-310001969373vtmx:OperatingParkPIQQueretaroMember2023-12-310001969373vtmx:OperatingParkVPQueretaroQueretaroMember2023-01-012023-12-310001969373vtmx:OperatingParkVPQueretaroQueretaroMember2023-12-310001969373vtmx:OperatingParkQueretaroAerospaceParkQueretaroAeroMember2023-01-012023-12-310001969373vtmx:OperatingParkQueretaroAerospaceParkQueretaroAeroMember2023-12-310001969373vtmx:OperatingParkSMASanMiguelDeAllendMember2023-01-012023-12-310001969373vtmx:OperatingParkSMASanMiguelDeAllendMember2023-12-310001969373vtmx:OperatingParkLasColinasSilaoMember2023-01-012023-12-310001969373vtmx:OperatingParkLasColinasSilaoMember2023-12-310001969373vtmx:OperatingParkVestaParkPuertoInteriorSilaoMember2023-01-012023-12-310001969373vtmx:OperatingParkVestaParkPuertoInteriorSilaoMember2023-12-310001969373vtmx:OperatingParkTresNacionesSLPMember2023-01-012023-12-310001969373vtmx:OperatingParkTresNacionesSLPMember2023-12-310001969373vtmx:OperatingParkVestaParkSLPSanLuisPotosiMember2023-01-012023-12-310001969373vtmx:OperatingParkVestaParkSLPSanLuisPotosiMember2023-12-310001969373vtmx:OperatingParkLaMesaVestaParkTijuanaMember2023-01-012023-12-310001969373vtmx:OperatingParkLaMesaVestaParkTijuanaMember2023-12-310001969373vtmx:OperatingParkNordikaTijuanaMember2023-01-012023-12-310001969373vtmx:OperatingParkNordikaTijuanaMember2023-12-310001969373vtmx:OperatingParkElPotreroTijuanaMember2023-01-012023-12-310001969373vtmx:OperatingParkElPotreroTijuanaMember2023-12-310001969373vtmx:OperatingParkVestaParkTijuanaIIITijuanaMember2023-01-012023-12-310001969373vtmx:OperatingParkVestaParkTijuanaIIITijuanaMember2023-12-310001969373vtmx:OperatingParkVestaParkPacificoTijuanaMember2023-01-012023-12-310001969373vtmx:OperatingParkVestaParkPacificoTijuanaMember2023-12-310001969373vtmx:OperatingParkVPLagoEsteTijuanaMember2023-01-012023-12-310001969373vtmx:OperatingParkVPLagoEsteTijuanaMember2023-12-310001969373vtmx:OperatingParkVestaParkMegaregionTijuanaMember2023-01-012023-12-310001969373vtmx:OperatingParkVestaParkMegaregionTijuanaMember2023-12-310001969373vtmx:OperatingParkVPTITlaxcalaMember2023-01-012023-12-310001969373vtmx:OperatingParkVPTITlaxcalaMember2023-12-310001969373vtmx:OperatingParkExportecTolucaMember2023-01-012023-12-310001969373vtmx:OperatingParkExportecTolucaMember2023-12-310001969373vtmx:OperatingParkT2000TolucaMember2023-01-012023-12-310001969373vtmx:OperatingParkT2000TolucaMember2023-12-310001969373vtmx:OperatingParkElCoecilloVestaParkTolucaMember2023-01-012023-12-310001969373vtmx:OperatingParkElCoecilloVestaParkTolucaMember2023-12-310001969373vtmx:OperatingParkVestaParkTolucaITolucaMember2023-01-012023-12-310001969373vtmx:OperatingParkVestaParkTolucaITolucaMember2023-12-310001969373vtmx:OperatingParkVestaParkApodacaMonterreyMember2023-01-012023-12-310001969373vtmx:OperatingParkVestaParkApodacaMonterreyMember2023-12-310001969373vtmx:OperatingParkPARQUELASVENTANASMatamorosMember2023-01-012023-12-310001969373vtmx:OperatingParkPARQUELASVENTANASMatamorosMember2023-12-310001969373vtmx:OperatingParkVESTAPARKALAMARTijuanaMember2023-01-012023-12-310001969373vtmx:OperatingParkVESTAPARKALAMARTijuanaMember2023-12-310001969373vtmx:OperatingParkVESTAPARKRIVERALARA1CdJuarezMember2023-01-012023-12-310001969373vtmx:OperatingParkVESTAPARKRIVERALARA1CdJuarezMember2023-12-310001969373vtmx:OperatingParkVESTAPARKROSARITO1TijuanaMember2023-01-012023-12-310001969373vtmx:OperatingParkVESTAPARKROSARITO1TijuanaMember2023-12-310001969373vtmx:OperatingParkVESTALAGOSMORENOLagosMember2023-01-012023-12-310001969373vtmx:OperatingParkVESTALAGOSMORENOLagosMember2023-12-310001969373vtmx:OperatingParkVESTATLAXCALATlaxcalaMember2023-01-012023-12-310001969373vtmx:OperatingParkVESTATLAXCALATlaxcalaMember2023-12-310001969373vtmx:OperatingParkVESTAMORELOSTijuanaMember2023-01-012023-12-310001969373vtmx:OperatingParkVESTAMORELOSTijuanaMember2023-12-310001969373vtmx:OperatingParkSTELLANTISITolucaMember2023-01-012023-12-310001969373vtmx:OperatingParkSTELLANTISITolucaMember2023-12-310001969373vtmx:OperatingParkOtherMember2023-01-012023-12-310001969373vtmx:OperatingParkOtherMember2023-12-310001969373vtmx:OperatingParksMember2023-01-012023-12-310001969373vtmx:OperatingParksMember2023-12-310001969373vtmx:LandAndBuildingsUnderConstructionVestaParkJuarezOrienteCd.JuarezMember2023-01-012023-12-310001969373vtmx:LandAndBuildingsUnderConstructionVestaParkJuarezOrienteCd.JuarezMember2023-12-310001969373vtmx:LandAndBuildingsUnderConstructionVestaParkAguascalientesAguascalientesMember2023-01-012023-12-310001969373vtmx:LandAndBuildingsUnderConstructionVestaParkAguascalientesAguascalientesMember2023-12-310001969373vtmx:LandAndBuildingsUnderConstructionVestaParkSLPSanLuisPotosiMember2023-01-012023-12-310001969373vtmx:LandAndBuildingsUnderConstructionVestaParkSLPSanLuisPotosiMember2023-12-310001969373vtmx:LandAndBuildingsUnderConstructionTresNacionesSanLuisPotosiMember2023-01-012023-12-310001969373vtmx:LandAndBuildingsUnderConstructionTresNacionesSanLuisPotosiMember2023-12-310001969373vtmx:LandAndBuildingsUnderConstructionVPQueretaroQueretaroMember2023-01-012023-12-310001969373vtmx:LandAndBuildingsUnderConstructionVPQueretaroQueretaroMember2023-12-310001969373vtmx:LandAndBuildingsUnderConstructionOtherValleDeMexicoMember2023-01-012023-12-310001969373vtmx:LandAndBuildingsUnderConstructionOtherValleDeMexicoMember2023-12-310001969373vtmx:LandAndBuildingsUnderConstructionMember2023-01-012023-12-310001969373vtmx:LandAndBuildingsUnderConstructionMember2023-12-310001969373vtmx:LandReservesVPSLPSanLuisPotosiMember2023-12-310001969373vtmx:LandReservesVPSLPSanLuisPotosiMember2023-01-012023-12-310001969373vtmx:LandReservesVPQueretaroQueretaroMember2023-12-310001969373vtmx:LandReservesVPQueretaroQueretaroMember2023-01-012023-12-310001969373vtmx:LandReservesVestaParkPuertoInteriorSilaoMember2023-12-310001969373vtmx:LandReservesVestaParkPuertoInteriorSilaoMember2023-01-012023-12-310001969373vtmx:LandReservesVestaParkAguascalientesAguascalientesMember2023-12-310001969373vtmx:LandReservesVestaParkAguascalientesAguascalientesMember2023-01-012023-12-310001969373vtmx:LandReservesVestaPueblaIIPueblaMember2023-12-310001969373vtmx:LandReservesVestaPueblaIIPueblaMember2023-01-012023-12-310001969373vtmx:LandReservesSMASanMiguelDeAllendeMember2023-12-310001969373vtmx:LandReservesSMASanMiguelDeAllendeMember2023-01-012023-12-310001969373vtmx:LandReservesVestaParkApodacaMonterreyMember2023-12-310001969373vtmx:LandReservesVestaParkApodacaMonterreyMember2023-01-012023-12-310001969373vtmx:LandReservesMember2023-12-310001969373vtmx:LandReservesMember2023-01-012023-12-3100019693732016-01-012017-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

| | | | | |

| o | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2023 |

OR |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from __________ to __________. |

OR |

| o | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| Date of event requiring this shell company report ________________ |

Commission file number: 001-41730

Corporación Inmobiliaria Vesta, S.A.B. de C.V.

(Exact name of Registrant as specified in its charter)

Vesta Real Estate Corporation, S.A.B. de C.V.

(Translation of Registrant’s name into English)

Mexico

(Jurisdiction of incorporation or organization)

Paseo de los Tamarindos No. 90,

Torre II, Piso 28, Col. Bosques de las

Lomas

Cuajimalpa, C.P. 5120

Mexico City

United Mexican States

+52 (55) 5950-0070

(Address of principal executive offices)

Juan Felipe Sottil Achutegui

Chief Financial Officer

Paseo de los Tamarindos No. 90,

Torre II, Piso 28, Col. Bosques de las

Lomas

Cuajimalpa, C.P. 5120

Mexico City

United Mexican States

+52 (55) 5950-0070

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

American Depositary Shares, each representing ten ordinary shares with no par value per share | | VTMX | | New York Stock Exchange |

Ordinary Shares, no par value per share* | | N/A | | New York Stock Exchange |

_____________________________

* Not for trading, but only in connection with the registration of the American Depositary Shares.

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

As of December 31, 2023, 884,486,436 ordinary shares were outstanding.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Note —Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) o

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) o

Indicate by check mark whether the registrant has submitted electronically, every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.:

| | | | | | | | | | | | | | | | | | | | |

| Large Accelerated Filer | o | Accelerated Filer | o | Non-accelerated Filer | x |

| | | | | Emerging growth company | x |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. o

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b) by the registered public accounting firm that prepared or issued its audit report. o

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| | | | | | | | |

| o | U.S. GAAP |

| x | International Financial Reporting Standards as issued by the International Accounting Standards Board |

| o | Other |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

[APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS]

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

TABLE OF CONTENTS

ABOUT THIS ANNUAL REPORT AND GLOSSARY OF CERTAIN TERMS AND DEFINITIONS

Except where the context otherwise requires or where otherwise indicated, the terms “Vesta,” “VTMX,” the “Company,” “Group,” “we,” “us,” “our,” “our company” and “our business” refer to Corporacion Inmobiliaria Vesta, S.A.B. de C.V., together with its consolidated subsidiaries as a consolidated entity.

All references in this Annual Report to the “Commission” or to the “SEC” are to the United States Securities and Exchange Commission, to the “Exchange Act” are to the U.S. Securities Exchange Act of 1934, as amended, and to the “Securities Act” are to the U.S. Securities Act of 1933, as amended.

In addition, set forth below is a glossary of certain industry and other terms used in this Annual Report:

“Adjusted EBITDA” means the sum of profit for the period adjusted by (a) total income tax expense, (b) interest income, (c) other income, (d) other expense, (e) finance costs, (f) exchange gain (loss) – net, (g) gain on sale of investment property, (h) gain on revaluation of investment property, (i) depreciation and (j) stock-based compensation, (k) energy income and (l) energy costs during the relevant period.

“Adjusted NOI” means the sum of NOI plus property operating costs related to properties that did not generate rental income during the relevant period.

“AMVO” means the Asociación Mexicana de Venta Online (Mexican Association of Online Sales).

“BMV” means the Bolsa Mexicana de Valores, S.A.B. de C.V. (Mexican Stock Exchange).

“BTS Building” means a build-to-suit building that is designed and constructed in a tailor-made manner in order to meet client-specific needs.

“CETES” means the Mexican Certificados de la Tesorería de la Federación (Federal Treasury Certificates).

“Class A Buildings” are industrial properties that typically possess most of the following characteristics: (i) 15 years old or newer; (ii) concrete tilt-up construction; (iii) clear height in excess of 26 feet, (iv) a ratio of dock doors to floor area that is more than one door per 10,000 square feet; and (v) energy efficient design characteristics suitable for current and future tenants.

“CNBV” means the Mexican Comisión Nacional Bancaria y de Valores (Mexican National Banking and Securities Commission).

“CPA” means Corporate Properties of the Americas.

“CPI” means the U.S. Consumer Price Index.

“CPW” means CPW México, S. de R.L. de C.V.

“Federal Government” means the Federal Government of Mexico.

“FFO” means profit for the period, excluding: (i) gain on sale of investment property and (ii) gain on revaluation of investment property.

“General Electric” means G.E. Real Estate de México, S. de R.L. de C.V.

“GLA” means gross leasable area.

“IASB” means the International Accounting Standards Board.

“IFRS” means International Financial Reporting Standards, as issued by the IASB.

“Indeval” means S.D. Indeval Institución para el Depósito de Valores, S. A. de C.V.

“INEGI” means the Mexican Instituto Nacional de Estadística y Geografía (Mexican National Institute of Statistics and Geography).

“INPC” means the Mexican Índice Nacional de Precios al Consumidor (Mexican National Consumer Price Index).

“Inventory Buildings” are buildings that are built without a lease signed with a specific customer, and designed in accordance with standard industry specifications, for the purpose of having readily-available space for clients that do not have the time or interest to build a specialized BTS Building.

“Land Reserves” means the lots of land acquired and maintained for future development into leasable properties.

“LEED Certification” means a certification granted by the Leadership in Energy and Environmental Design, which certifies a building’s compliance with certain environmental standards.

“LTV” means loan-to-value, which represents a real estate information ratio that measures debt value over asset value.

“Mexican Central Bank” means the Banco de México (Bank of Mexico).

“Multi-Tenant Buildings” means buildings designed and built pursuant to general specifications and which may be adapted for two or more tenants, each with its specific GLA and separate entrances and utilities.

“Net Debt to Adjusted EBITDA” means (i) our gross debt (defined as current portion of long-term debt plus long-term debt plus amortization of debt issuance costs) less cash and cash equivalents divided by (ii) Adjusted EBITDA.

“Net Debt to Total Assets” means (i) our gross debt (defined as current portion of long-term debt plus long-term debt plus amortization of debt issuance costs) less cash and cash equivalents divided by (ii) total assets.

“Nissan” means Nissan Mexicana, S.A. de C.V.

“Nissan Trust” means the trust agreement dated July 5, 2013, between Nissan, as trustor and beneficiary, and Vesta DSP, as trustor and beneficiary, and formerly by Deutsche Bank Mexico, S.A., Multiple Banking Institution, (currently, CIBanco, S.A., Institución de Banca Múltiple, as successor), as trustee, as such has been or is amended from time to time, pursuant to which the terms and conditions for the development of Vesta DSP (as defined below) were established.

“NOI” means the sum of Adjusted EBITDA plus general and administrative expenses, minus long-term incentive plan and equity plus during the relevant period.

“Paris Agreement” means the international agreement on climate change that is legally binding in the United Nations Framework Convention on Climate Change (UNFCCC) on climate change mitigation, adaptation, and finance.

“PCAOB” means the U.S. Public Company Accounting Oversight Board.

“PROFEPA” means the Mexican Procuraduría Federal de Protección al Ambiente (Mexican Federal Environmental Protection Agency).

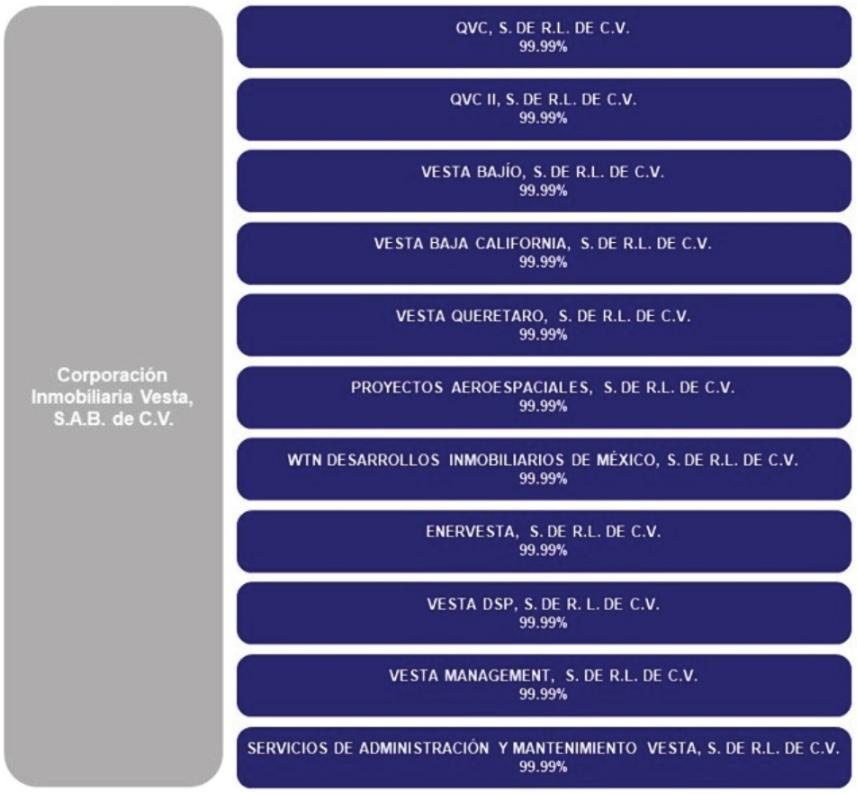

“Proyectos Aeroespaciales” means Proyectos Aeroespaciales, S. de R.L. de C.V., a subsidiary of Vesta.

“PTS Park” means an industrial park-to-suit that is designed and constructed in a tailor-made manner in order to meet specific needs of an industry or cluster.

“REIT” means real estate investment trust.

“Securities Act” means the U.S. Securities Act of 1933, as amended.

“TPI” means TPI Composites, S. de R.L. de C.V.

“QAP” means the Querétaro Aerospace Park.

“QVC” means QVC, S. de R.L. de C.V., a subsidiary of Vesta.

“QVC II” means QVC II, S. de R.L. de C.V., a subsidiary of Vesta.

“QVC III” means QVC III, S. de R.L. de C.V.

“RNV” means the Mexican Registro Nacional de Valores (Mexican National Securities Registry).

“Same-Store NOI” means rental income of Same-Store Properties in a period minus property operating costs related to such properties. This provides a further analysis of Adjusted NOI by providing the operating performance from the population of properties that is consistent from period to period.

“Same-Store Properties” means properties that we have owned for the entirety of the applicable period and the comparable period and that have reported at least twelve months reaching GLA occupancy of 80.0% in relation to total GLA of such property or had been completed for more than one year, whichever occurs first.

“SEDI” means the Sistema Electrónico de Envío y Difusión de Información (automated electronic information transfer system).

“USMCA” means the United States-Mexico-Canada Agreement which entered into force on July 1, 2020.

“VBC” means Vesta Baja California, S. de R.L. de C.V., a subsidiary of Vesta.

“Vesta DSP” means Vesta DSP, S. de R.L. de C.V., a subsidiary of Vesta.

“Vesta FFO” means the sum of FFO, as adjusted for the impact of exchange gain (loss) – net, other income - net, interest income, total income tax expense, depreciation and long-term incentive plan and equity plus.

“Vesta Management” means Vesta Management, S. de R.L. de C.V., a subsidiary of Vesta.

“WTN” means WTN Desarrollos Inmobiliarios de México, S. de R.L. de C.V., a subsidiary of Vesta.

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

We report under International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (the “IASB”). None of our financial statements were prepared in accordance with generally accepted accounting principles in the United States (“U.S. GAAP”). We present our consolidated financial statements in U.S. dollars. This annual report does not include a reconciliation of IFRS to U.S. GAAP. You should consult your own professional advisers for an understanding of the differences between IFRS and U.S. GAAP, and how those differences might affect the financial information included in this annual report. Per share amounts are presented based on the weighted average number of ordinary shares outstanding. For more information, see note 12.5 to our audited consolidated financial statements.

Appraisals

We use independent external appraisers to determine the fair value of our investment properties. Such appraisers use different valuation methodologies (including discounted cash flow analysis, replacement cost and income capitalization analysis) that include assumptions that are not directly observable in the market (such as discount rates, exit cap rates, long-term NOI, inflation rates, absorption periods and market rents) to determine a projected NOI and the market value of our investment assets. This property-by-property valuation is carried out on a quarterly basis. The main valuation method used by the external appraisers is the discounted cash flow analysis for properties and market value to determine the value of our Land Reserves.

Our financial statements included with this annual report contain a detailed description of the valuation of our properties.

Our management believes that the independent appraisal process and the chosen valuation methodologies as well as the assumptions used under such methodologies are appropriate for determining the fair value of the type of investment properties we own. For more information about the procedures that we perform to validate the independent appraisals, see “Operating and Financial Review and Prospects—Critical Accounting Estimates—Valuation of Investment Property.”

Special Note Regarding Non-IFRS Financial Measures and Other Measures

Non-IFRS financial measures do not follow generally accepted accounting principles and, as such, do not follow IFRS. In this Annual Report, we report our Adjusted EBITDA, NOI, Adjusted NOI, FFO, Vesta FFO, Net Debt to Adjusted EBITDA, Net Debt to Total Assets and Same-Store NOI. These non-IFRS measures, however, do not have standardized meanings and may not be directly comparable to similarly-titled measures adopted by other companies. Potential investors should not rely on information not recognized under IFRS as a substitute for the IFRS measures of earnings or liquidity in making an investment decision.

We calculate Adjusted EBITDA as the sum of profit for the period adjusted by (a) total income tax expense (b) interest income, (c) other income, (d) other expense, (e) finance costs, (f) exchange gain (loss) – net, (g) gain on sale of investment property, (h) gain on revaluation of investment property, (i) depreciation, (j) stock-based compensation, (k) energy income and (l) energy costs during the relevant period. We calculate NOI as the sum of Adjusted EBITDA plus general and administrative expenses, minus depreciation and stock-based compensation during the relevant period. We calculate Adjusted NOI as the sum of NOI plus property operating costs related to properties that did not generate rental income during the relevant period.

Adjusted EBITDA is not a financial measure recognized under IFRS and does not purport to be an alternative to profit or total comprehensive income for the period as a measure of operating performance or to cash flows from operating activities as a measure of liquidity. Additionally, Adjusted EBITDA is not intended to be a measure of free cash flow available for management’s discretionary use, as it does not consider certain cash requirements such as interest payments and tax payments. Our presentation of Adjusted EBITDA has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our results as reported under IFRS. Management uses Adjusted EBITDA to measure and evaluate the operating performance of our principal business (which consists of developing, leasing and managing industrial properties) before our cost of capital and income tax expense. Adjusted EBITDA is a measure commonly used in our industry, and we present Adjusted EBITDA to supplement investor understanding of our operating performance. We believe that Adjusted EBITDA provides investors and analysts with a measure of operating results unaffected by differences in capital structures, capital investment cycles and fair value adjustments of related assets among otherwise comparable companies.

NOI or Adjusted NOI are not financial measures recognized under IFRS and do not purport to be alternatives to profit for the period or total comprehensive income as measures of operating performance. NOI and Adjusted NOI are

supplemental industry reporting measures used to evaluate the performance of our investments in real estate assets and our operating results. In addition, Adjusted NOI is a leading indicator of the trends related to NOI as we typically have a strong development portfolio of “speculative buildings.” Under IAS 40, we have adopted the fair value model to measure our investment property and, for that reason, our financial statements do not reflect depreciation nor amortization of our investment properties, and therefore such items are not part of the calculations of NOI or Adjusted NOI. We believe that NOI is useful to investors as a performance measure and that it provides useful information regarding our results of operations and financial condition because, when compared across periods, it reflects the impact on operations from trends in occupancy rates, rental rates, operating costs and acquisition and development activity on an unleveraged basis, providing perspective not immediately apparent from profit for the year. For example, interest expense is not necessarily linked to the operating performance of a real estate asset and is often incurred at the corporate level as opposed to the property level. Similarly, interest expense may be incurred at the property level even though the financing proceeds may be used at the corporate level (e.g., used for other investment activity). As so defined, NOI and Adjusted NOI may not be comparable to net operating income or similar measures reported by other real estate companies that define NOI or Adjusted NOI differently.

FFO is calculated as profit for the period, excluding: (i) gain on sale of investment property and (ii) gain on revaluation of investment property. We calculate Vesta FFO as the sum of FFO, as adjusted for the impact of exchange gain (loss) – net, other income, other expense, interest income, total income tax expense, depreciation and stock-based compensation, energy income and energy costs.

The Company believes that Vesta FFO is useful to investors as a supplemental performance measure because it excludes the effects of certain items which can create significant earnings volatility, but which do not directly relate to our business operations. We believe Vesta FFO can facilitate comparisons of operating performance between periods, while also providing a more meaningful predictor of future earnings potential.

Additionally, since Vesta FFO does not capture the level of capital expenditures per maintenance and improvements to maintain the operating performance of properties, which has a material economic impact on operating results, we believe Vesta FFO’s usefulness as a measure of performance may be limited.

Our computation of FFO and Vesta FFO may not be comparable to FFO measures reported by other REITs or real estate companies that define or interpret the FFO definition differently. FFO and Vesta FFO should not be considered as a substitute for net profit for the period attributable to our common shareholders.

We compute FFO and Vesta FFO per share amounts using the weighted average number of ordinary shares outstanding during the relevant period. For more information, see note 12.5 to our audited consolidated financial statements.

Net Debt to Adjusted EBITDA represents (i) our gross debt (defined as current portion of long-term debt plus long-term debt plus amortization of debt issuance costs) less cash and cash equivalents divided by (ii) Adjusted EBITDA. Our management believes that this ratio is useful because it provides investors with information on our ability to repay debt, compared to our performance as measured using Adjusted EBITDA.

Net Debt to Total Assets represents (i) our gross debt (defined as current portion of long-term debt plus long-term debt plus amortization of debt issuance costs) less cash and cash equivalents divided by (ii) total assets. Our management believes that this ratio is useful because it shows the degree in which net debt has been used to finance our assets and using this measure investors and analysts can compare the leverage shown by this ratio with that of other companies in the same industry.

We present Same-Store NOI. We determine our Same-Store Properties at the end of each reporting period. Our same store population includes properties that were owned during the comparable period and that have reported at least twelve months of consecutive stabilized operations. We define “stabilized operations” as properties that have reached GLA occupancy of 80.0% in relation to total GLA of such property or that have been completed for more than one year, whichever occurs first.

The Same-Store Properties population is adjusted to remove properties that were sold or entered development subsequent to the beginning of the current period. As such, the “same store” population for the period ended December 31, 2023 includes all properties that had reached twelve months of “stabilized operations” by December 31, 2022.

We calculate Same-Store NOI as rental income for the same store population less the related property operating costs related to properties that generated rental income. We evaluate the performance of the properties we own using a Same-

Store NOI, and we believe that Same-Store NOI is helpful to investors and management as a supplemental performance measure because it includes the operating performance from the population of properties that is consistent from period to period, thereby eliminating the effects of changes in the composition of our portfolio on performance measures.

When used in conjunction with IFRS financial measures, Same-Store NOI is a supplemental measure of operating performance that we believe is a useful measure to evaluate the performance and profitability of our investment properties. Additionally, Same-Store NOI is a key metric used internally by our management to develop internal budgets and forecasts, as well as to assess the performance of our investment properties relative to budget and against prior periods. We believe presentation of Same-Store NOI provides investors with a supplemental view of our operating performance that can provide meaningful insights to the underlying operating performance of our investment properties, as these measures depict the operating results that are directly impacted by our investment properties and is consistent period over period and exclude items that may not be indicative of, or are unrelated to, the ongoing operations of such investment properties. It may also assist investors to evaluate our performance relative to peers of various sizes and maturities and provides greater transparency with respect to how our management evaluates our business, as well as our financial and operational decision-making.

For reconciliations of Adjusted EBITDA, NOI and Adjusted NOI to profit for the period, FFO and Vesta FFO to profit for the period, Net Debt to total debt, see Item 5A. “Operating and Financial Review and Prospects—Operating Results—Non-IFRS Financial Measures and Other Measures and Reconciliations.”

Currency and Other Information

Unless otherwise stated, the financial information appearing in this Annual Report is presented in U.S. dollars. In this Annual Report references to “peso,” “pesos” or “Ps.” are to Mexican pesos, and references to “U.S. dollar,” “U.S. dollars,” “dollar,” “dollars” or “US$” are to United States dollars.

The U.S. dollar is the functional currency of Vesta and all of its subsidiaries except for WTN, which considers the peso to be its functional currency, for which reason WTN is considered to be a “foreign operation” under IFRS. A “foreign operation” is an entity that is a subsidiary, associate, joint arrangement or branch of a reporting entity, the activities of which are based or conducted in a country or currency other than those of the reporting entity.

For purposes of presenting consolidated financial statements, the assets and liabilities of WTN are translated into U.S. dollars using the exchange rates in effect on the last business day of each reporting period. Income and expense items are translated at the average exchange rates for the period, unless exchange rates fluctuate significantly during that period, in which case the exchange rates in effect on the dates of the transactions are used. Exchange differences arising, if any, are recorded in “other comprehensive income.”

Totals in some tables in this Annual Report may differ from the sum of individual amounts in those tables due to rounding. In this Annual Report, where information is presented in thousands, millions or billions of pesos or thousands, millions or billions of U.S. dollars, amounts of less than one thousand, one million, or one billion, as the case may be, have been truncated unless otherwise specified. All percentages have been rounded to the nearest percent, one-tenth of one percent or one-hundredth of one percent, as the case may be. In some cases, amounts and percentages presented in tables in this Annual Report may not add up due to such rounding adjustments or truncating.

Industry and Market Data

Certain market data and other statistical information (other than with respect to our financial results and performance) used in this Annual Report are based on independent industry publications, government publications, reports by market research firms or other published independent sources, including but not limited to INEGI, World Bank, U.S. Bureau of Economic Analysis (BEA), U.S. Economic Census Bureau, CBRE, CBRE Research, Bloomberg, Federal Reserve Bank of Dallas, Americas Market Intelligence, JLL, JLL Mexico, JLL Research, AMVO, Kearney, The Boston Consulting Group, the Mexican Ministry of Economy, the Mexican Central Bank, the Global Trade and Innovation Policy Alliance, Deloitte, International Organization of Motor Vehicle Manufacturers, Euromonitor, Organization for Economic Cooperation and Development, United Nations, Mexican Automotive Industry Association, National Association of Manufacturers, International Trade Administration, Optoro, Office of the U.S. Trade Representative, PGIM, Shipa Freight, Freight Qoute, Peterson Institute for International Economics, GBM, LENS, Cushman & Wakefield, International Monetary Fund, Interamerican Development Bank, and Statista.

Some data are also based on our estimates, which are derived from our review of internal surveys and analyses, as well as from independent sources. Although we believe these sources are reliable, we have not independently verified the

information and cannot guarantee their accuracy or completeness. In addition, these sources may use different definitions of the relevant markets than those we present. Data regarding our industry are intended to provide general guidance but are inherently imprecise. Though we believe these estimates were reasonably derived, you should not place undue reliance on estimates, as they are inherently uncertain. Nothing in this Annual Report should be interpreted as a market forecast.

The standard measures of area in the real estate market in Mexico are the square meter (m2) and the hectare (ha), while in the U.S. they are the square foot (ft2) and the acre (ac), respectively. This Annual Report contains information in both (i) square meters and square feet applying a conversion factor of 1 square meter = 10.8 square feet, and (ii) hectares and acres, applying a conversion factor of 1 hectare = 2.5 acres.

Occupancy Rate

When we refer to our occupancy rate generally, we refer to the rate of all our occupied properties. When we refer to our stabilized occupancy rate, we refer to the rate of occupied stabilized properties only. We deem a property to be stabilized once it has reached 80.0% occupancy or has been completed for more than one year, whichever occurs first. The occupancy rate is calculated as the ratio of rented GLA to the total amount of available GLA. We consider the occupancy rate to be an important measure of the anticipated cash flow of the portfolio, and as an indicator of management leasing performance and the markets demand for the portfolio. We consider the stabilized occupancy rate to be an important measure of the anticipated cash flow of the stabilized portfolio and an indicator of management leasing performance and the market’s demand for the stabilized portfolio. Incorporating newly developed properties into the portfolio does not impact our stabilized occupancy rate. Our stabilized occupancy rate, however, does not have a standardized meaning and may not be directly comparable to similarly-titled measures adopted by other companies.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements. Examples of such forward-looking statements include, but are not limited to: (i) statements regarding our results of operations and financial position; (ii) statements of plans, objectives or goals, including those related to our operations and to our pipeline of potential developments and acquisitions; and (iii) statements of assumptions underlying such statements. Words such as “aim,” “anticipate,” “believe,” “could,” “estimate,” “expect,” “forecast,” “guidance,” “intend,” “may,” “plan,” “potential,” “predict,” “seek,” “should,” “will” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements.

By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that the predictions, forecasts, projections and other forward-looking statements will not be achieved. We caution investors that a number of important factors could cause actual results to differ materially from the plans, objectives, expectations, estimates and intentions expressed or implied in such forward-looking statements, including the following factors:

•our business and strategy of investing in industrial facilities, which may subject us to risks of the sector in which we operate but uncommon to other companies that invest primarily in a broader range of real estate assets;

•our ability to maintain or increase our rental rates and occupancy rates;

•the performance and financial condition of our tenants;

•our expectations regarding income, expenses, sales, operations and profitability;

•our ability to obtain returns from our projects similar or comparable to those obtained in the past;

•our ability to successfully expand into new markets in Mexico;

•our ability to successfully engage in property development;

•our ability to lease or sell any of our properties;

•our ability to successfully acquire land or properties to be able to execute on our accelerated growth strategy;

•the competition within our industry and markets in which we operate;

•economic trends in the industries or the markets in which our customers operate;